Credit Suisse Investment Banking Pitch Book

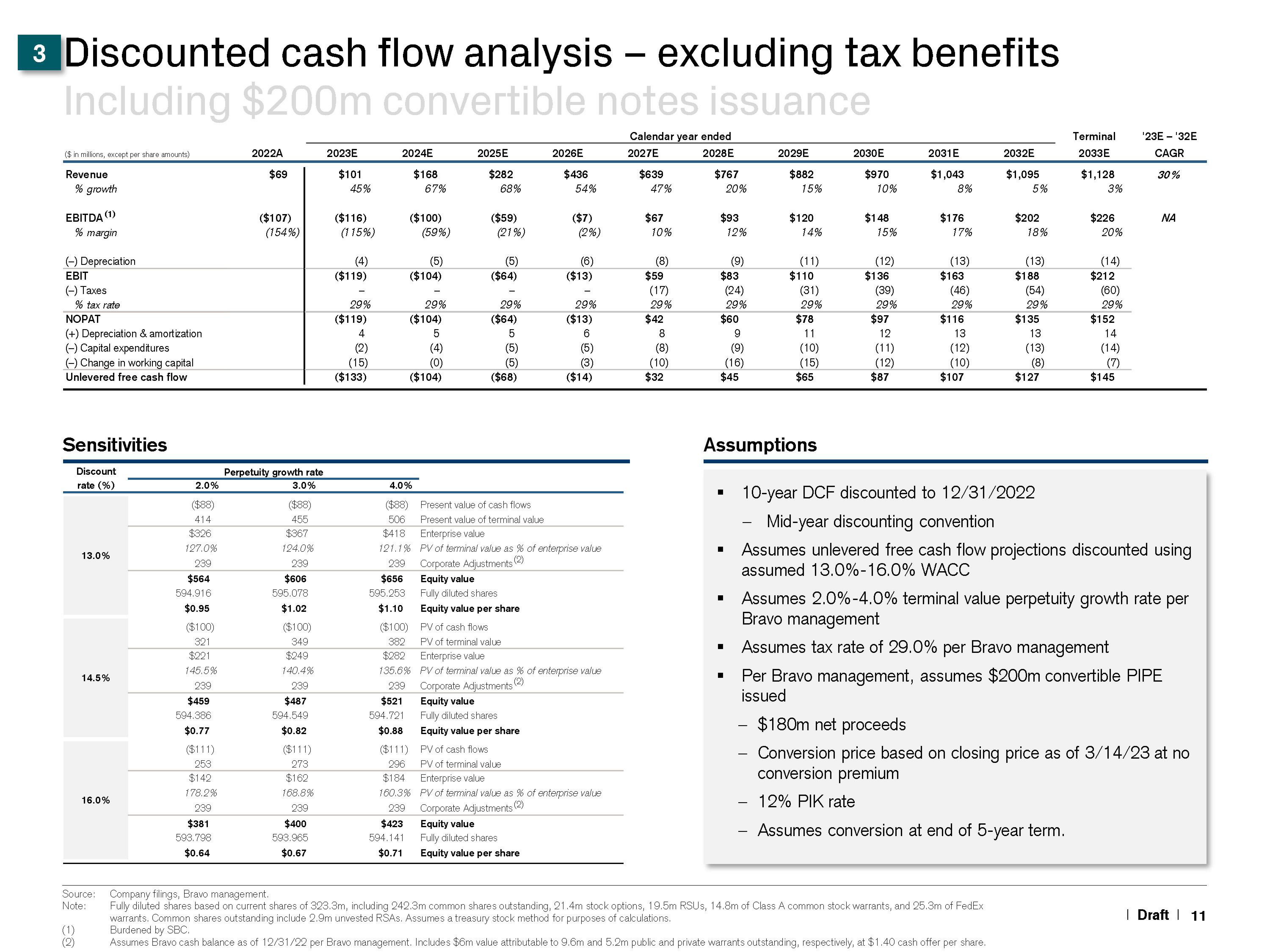

3 Discounted cash flow analysis - excluding tax benefits

Including $200m convertible notes issuance

Calendar year ended

2027E

2028E

($ in millions, except per share amounts)

Revenue

% growth

(1)

% margin

EBITDA

(-) Depreciation

EBIT

(-) Taxes

% tax rate

NOPAT

(+) Depreciation & amortization

(-) Capital expenditures

(-) Change in working capital

Unlevered free cash flow

Sensitivities

(1)

(2)

Discount

rate (%)

13.0%

14.5%

16.0%

Source:

Note:

2.0%

($88)

414

$326

127.0%

239

$564

594.916

$0.95

($100)

321

$221

145.5%

239

$459

594.386

$0.77

($111)

253

$142

178.2%

239

$381

593.798

$0.64

2022A

$69

($107)

(154%)

Perpetuity growth rate

3.0%

($88)

455

$367

124.0%

239

$606

595.078

$1.02

($100)

349

$249

140.4%

239

$487

594.549

$0.82

($111)

273

$162

168.8%

239

$400

593.965

$0.67

2023E

$101

45%

($116)

(115%)

(4)

($119)

29%

($119)

4

(2)

(15)

($133)

2024E

$656

595,253

$1.10

($100)

382

$282

$168

($111)

296

$184

67%

($100)

(59%)

594.141

$0.71

(5)

($104)

29%

($104)

5

(4)

(0)

($104)

2025E

$282

68%

($59)

$423 Equity value

(21%)

(5)

($64)

29%

($64)

5

(5)

(5)

($68)

Equity value

Fully diluted shares

Equity value per share

Equity value per share

2026E

4.0%

($88) Present value of cash flows

506

Present value of terminal value

$418

Enterprise value

121.1% PV of terminal value as % of enterprise value

239

Corporate Adjustments (2)

$436

54%

Fully diluted shares

Equity value per share

($7)

(2%)

PV of cash flows

PV of terminal value

Enterprise value

135.6% PV of terminal value as % of enterprise value

(2)

239 Corporate Adjustments

$521 Equity value

594.721 Fully diluted shares

$0.88

(6)

($13)

29%

($13)

6

(5)

(3)

($14)

PV of cash flows

PV of terminal value

Enterprise value

160.3% PV of terminal value as % of enterprise value

239 Corporate Adjustments (2)

$639

47%

$67

10%

(8)

$59

(17)

29%

$42

8

(8)

(10)

$32

$767

$93

20%

$83

12%

■

(9)

(24)

29%

$60

■

$45

■

9

(9)

(16)

2029E

$882

15%

$120

14%

(11)

$110

(31)

29%

Assumptions

$78

11

(10)

(15)

$65

2030E

$970

10%

$148

15%

(12)

$136

(39)

29%

$97

12

(11)

(12)

$87

2031E

$1,043

8%

$176

17%

(13)

$163

(46)

29%

$116

13

(12)

(10)

$107

2032E

$1,095

5%

$202

18%

(13)

Company filings, Bravo management.

Fully diluted shares based on current shares of 323.3m, including 242.3m common shares outstanding, 21.4m stock options, 19.5m RSUS, 14.8m of Class A common stock warrants, and 25.3m of FedEx

warrants. Common shares outstanding include 2.9m unvested RSAS. Assumes a treasury stock method for purposes of calculations.

Burdened by SBC.

Assumes Bravo cash balance as of 12/31/22 per Bravo management. Includes $6m value attributable to 9.6m and 5.2m public and private warrants outstanding, respectively, at $1.40 cash offer per share.

$188

(54)

29%

$135

13

(13)

(8)

$127

10-year DCF discounted to 12/31/2022

Mid-year discounting convention

Terminal

2033E

$1,128

3%

$226

20%

(14)

$212

(60)

29%

$152

14

(14)

(7)

$145

'23E-¹32E

CAGR

30%

ΝΑ

Assumes unlevered free cash flow projections discounted using

assumed 13.0%-16.0% WACC

Assumes 2.0% -4.0% terminal value perpetuity growth rate per

Bravo management

Assumes tax rate of 29.0% per Bravo management

Per Bravo management, assumes $200m convertible PIPE

issued

- $180m net proceeds

Conversion price based on closing price as of 3/14/23 at no

conversion premium

12% PIK rate

Assumes conversion at end of 5-year term.

| Draft | 11View entire presentation