Cyxtera SPAC Presentation Deck

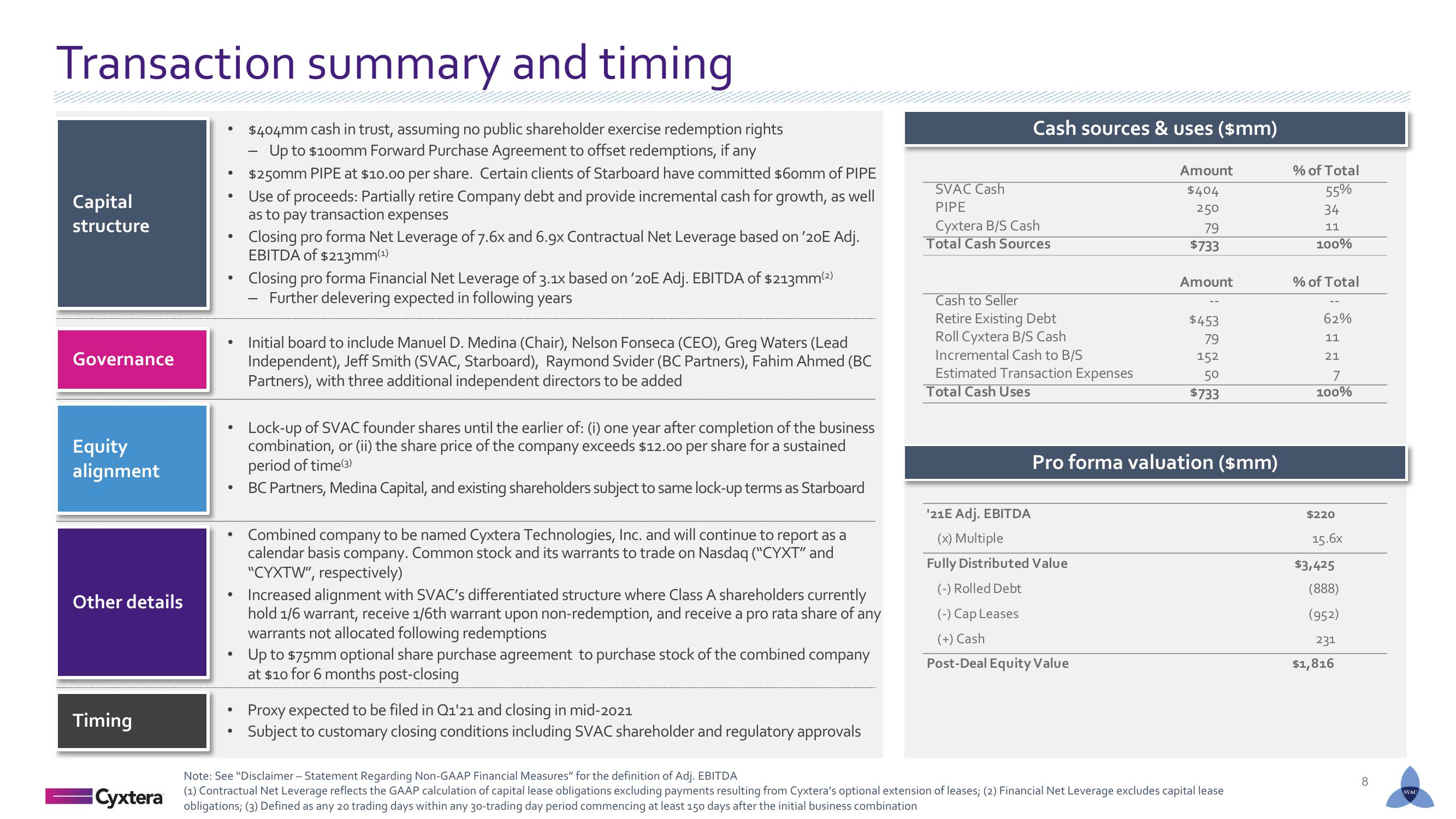

Transaction summary and timing

Capital

structure

Governance

Equity

alignment

Other details

Timing

Cyxtera

●

●

●

.

●

●

●

$404mm cash in trust, assuming no public shareholder exercise redemption rights

Up to $100mm Forward Purchase Agreement to offset redemptions, if any

$250mm PIPE at $10.00 per share. Certain clients of Starboard have committed $60mm of PIPE

Use of proceeds: Partially retire Company debt and provide incremental cash for growth, as well

as to pay transaction expenses

Closing pro forma Net Leverage of 7.6x and 6.9x Contractual Net Leverage based on '20E Adj.

EBITDA of $213mm(¹)

Closing pro forma Financial Net Leverage of 3.1x based on '20E Adj. EBITDA of $213mm(²)

Further delevering expected in following years

-

Initial board to include Manuel D. Medina (Chair), Nelson Fonseca (CEO), Greg Waters (Lead

Independent), Jeff Smith (SVAC, Starboard), Raymond Svider (BC Partners), Fahim Ahmed (BC

Partners), with three additional independent directors to be added

Lock-up of SVAC founder shares until the earlier of: (i) one year after completion of the business

combination, or (ii) the share price of the company exceeds $12.00 per share for a sustained

period of time (3)

BC Partners, Medina Capital, and existing shareholders subject to same lock-up terms as Starboard

Combined company to be named Cyxtera Technologies, Inc. and will continue to report as a

calendar basis company. Common stock and its warrants to trade on Nasdaq ("CYXT" and

"CYXTW", respectively)

Increased alignment with SVAC's differentiated structure where Class A shareholders currently

hold 1/6 warrant, receive 1/6th warrant upon non-redemption, and receive a pro rata share of any

warrants not allocated following redemptions

Up to $75mm optional share purchase agreement to purchase stock of the combined company

at $10 for 6 months post-closing

Proxy expected to be filed in Q1'21 and closing in mid-2021

Subject to customary closing conditions including SVAC shareholder and regulatory approvals

Cash sources & uses ($mm)

Amount

$404

250

79

$733

SVAC Cash

PIPE

Cyxtera B/S Cash

Total Cash Sources

Cash to Seller

Retire Existing Debt

Roll Cyxtera B/S Cash

Incremental Cash to B/S

Estimated Transaction Expenses

Total Cash Uses

Amount

'21E Adj. EBITDA

(x) Multiple

Fully Distributed Value

(-) Rolled Debt

(-) Cap Leases

(+) Cash

Post-Deal Equity Value

$453

79

152

50

$733

Pro forma valuation ($mm)

Note: See "Disclaimer - Statement Regarding Non-GAAP Financial Measures" for the definition of Adj. EBITDA

(1) Contractual Net Leverage reflects the GAAP calculation of capital lease obligations excluding payments resulting from Cyxtera's optional extension of leases; (2) Financial Net Leverage excludes capital lease

obligations; (3) Defined as any 20 trading days within any 30-trading day period commencing at least 150 days after the initial business combination

% of Total

55%

34

11

100%

% of Total

62%

11

21

7

100%

$220

15.6x

$3,425

(888)

(952)

231

$1,816

8

SVACView entire presentation