J.P.Morgan Investment Banking

APPENDIX

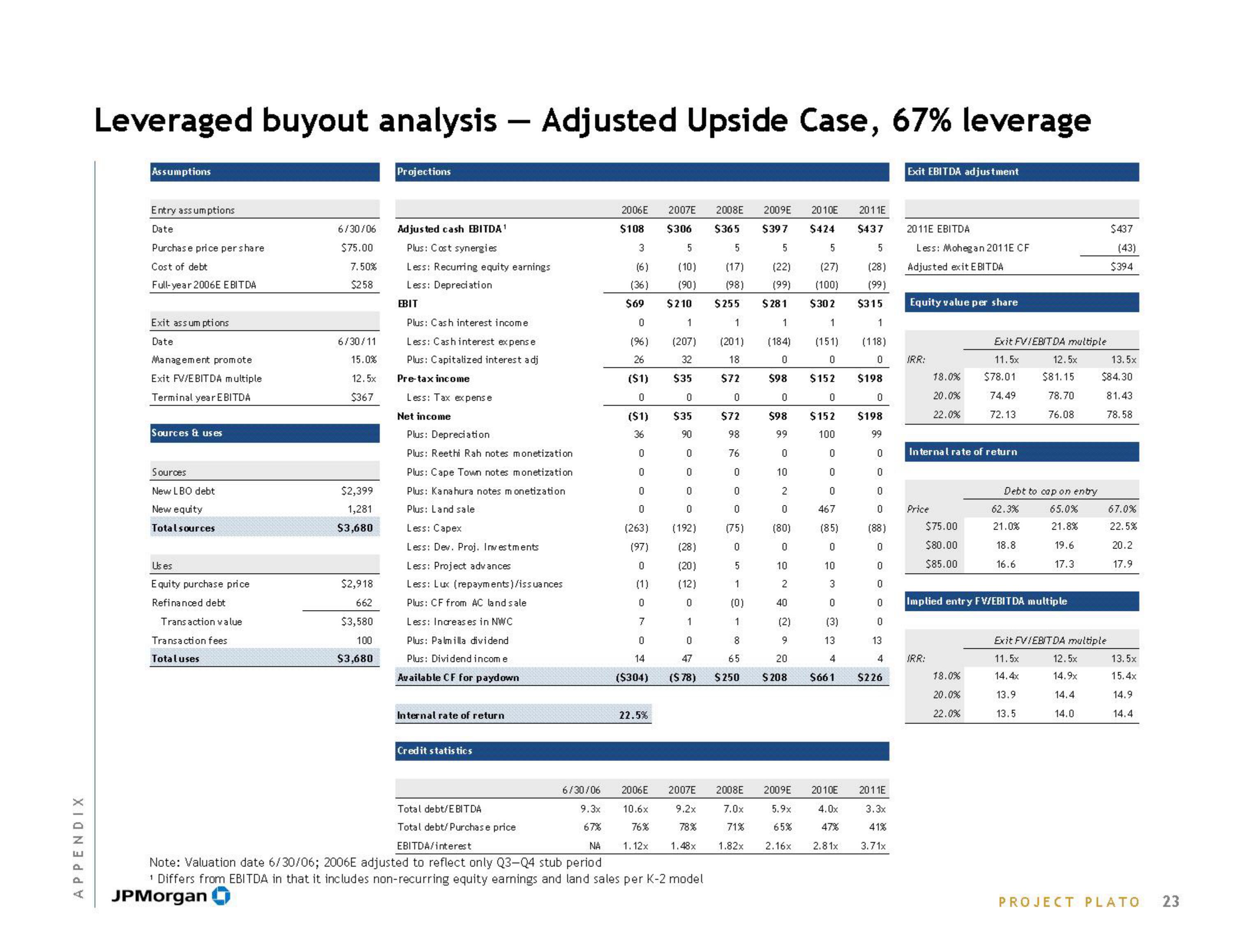

Leveraged buyout analysis - Adjusted Upside Case, 67% leverage

Assumptions

Entry assumptions

Date

Purchase price per share

Cost of debt

Full-year 2006E EBITDA

Exit ass um ptions

Date

Management promote

Exit FV/EBITDA multiple

Terminal year EBITDA

Sources & us es

Sources

New LBO debt

New equity

Total sources

Us es

Equity purchase price

Refinanced debt

Transaction value

Transaction fees

Totaluses

6/30/06

$75.00

7.50%

$258

6/30/11

15.0%

12.5x

$367

$2,399

1,281

$3,680

$2,918

662

$3,580

100

$3,680

Projections

Adjusted cash EBITDA¹

Plus: Cost synergies

Less: Recurring equity earnings

Less: Depreciatio

EBIT

Plus: Cash interest income

Less: Cash interest expense

Plus: Capitalized interest adj

Pre-tax income

Less: Tax expens e

Net income

Plus: Depreciation

Plus: Reethi Rah notes monetization

Plus: Cape Town notes monetization

Plus: Kanahura notes monetization

Plus: Land sale

Less: Capex

Less: Dev. Proj. Investments

Less: Project advances

Less: Lux (repayments)/issuances

Plus: CF from AC land sale

Less: Increases in NWC

Plus: Palmilla dividend

Plus: Dividend income

Available CF for paydown

Internal rate of return

Credit statistics

$108

2006E 2007E 2008E 2009E 2010E

$306 $365 $397 $424

5

5

5

5

(10) (17) (22) (27)

(90) (98) (99) (100)

$255 $281 $302

1

(36

$69 $210

0

1

1

(96) (207)

26

($1)

0

($1)

32

$35

0

$35

1

(201)

18

$72

0

$72

(184) (151)

0

$152 $198

0

$152

100

0

$98

0

$98

99

0

$198

99

36

90

98

76

0

0

0

0

0

0

0

(88)

0

0

0

0

0

13

Total debt/EBITDA

Total debt/Purchase price

3

(6)

0

0

0

0

(263)

(97)

0

(1)

0

7

0

14

($304)

22.5%

0

0

0

0

(192)

(28)

(20)

(12)

0

1

0

47

($ 78)

6/30/06

9.3x

67%

EBITDA/interest

NA

Note: Valuation date 6/30/06; 2006E adjusted to reflect only Q3-Q4 stub period

¹ Differs from EBITDA in that it includes non-recurring equity earnings and land sales per K-2 model

JPMorgan

2006E

2007E

9.2x

10.6x

76%

1.12x 1.48x

78%

0

0

0

(75)

0

5

1

(0)

1

8

65

$250

10

2

0

(80)

0

10

2

40

(2)

9

0

467

(85)

0

10

3

0

(3)

13

20

4

$208 $661

2008E 2009E

2010E

7.0x

5.9x

4.0x

71%

65%

47%

1.82x

2.16x 2.81x

2011E

$437

5

(28)

(99)

$315

1

(118)

0

4

$226

2011E

3.3x

41%

3.71x

Exit EBITDA adjustment

2011E EBITDA

Less: Mohegan 2011E CF

Adjusted exit EBITDA

Equity value per share

IRR:

Price

18.0%

20.0%

22.0%

Internal rate of return

$75.00

$80.00

$85.00

IRR:

Exit FVIEBITDA multiple

11.5x

$78.01

74.49

72.13

18.0%

20.0%

22.0%

12.5x

$81.15

78.70

76.08

Debt to cap on entry

65.0%

21.8%

19.6

17.3

62.3%

21.0%

18.8

16.6

Implied entry FV/EBITDA multiple

Exit FV/EBITDA multiple

11.5x

14.4x

13.9

13.5

12.5x

14.9x

14.4

14.0

$437

(43)

$394

13.5x

$84.30

81.43

78.58

67.0%

22.5%

20.2

17.9

13.5x

15.4x

14.9

14.4

PROJECT PLATO

23View entire presentation