J.P.Morgan Investment Banking Pitch Book

VALUATION SUMMARY

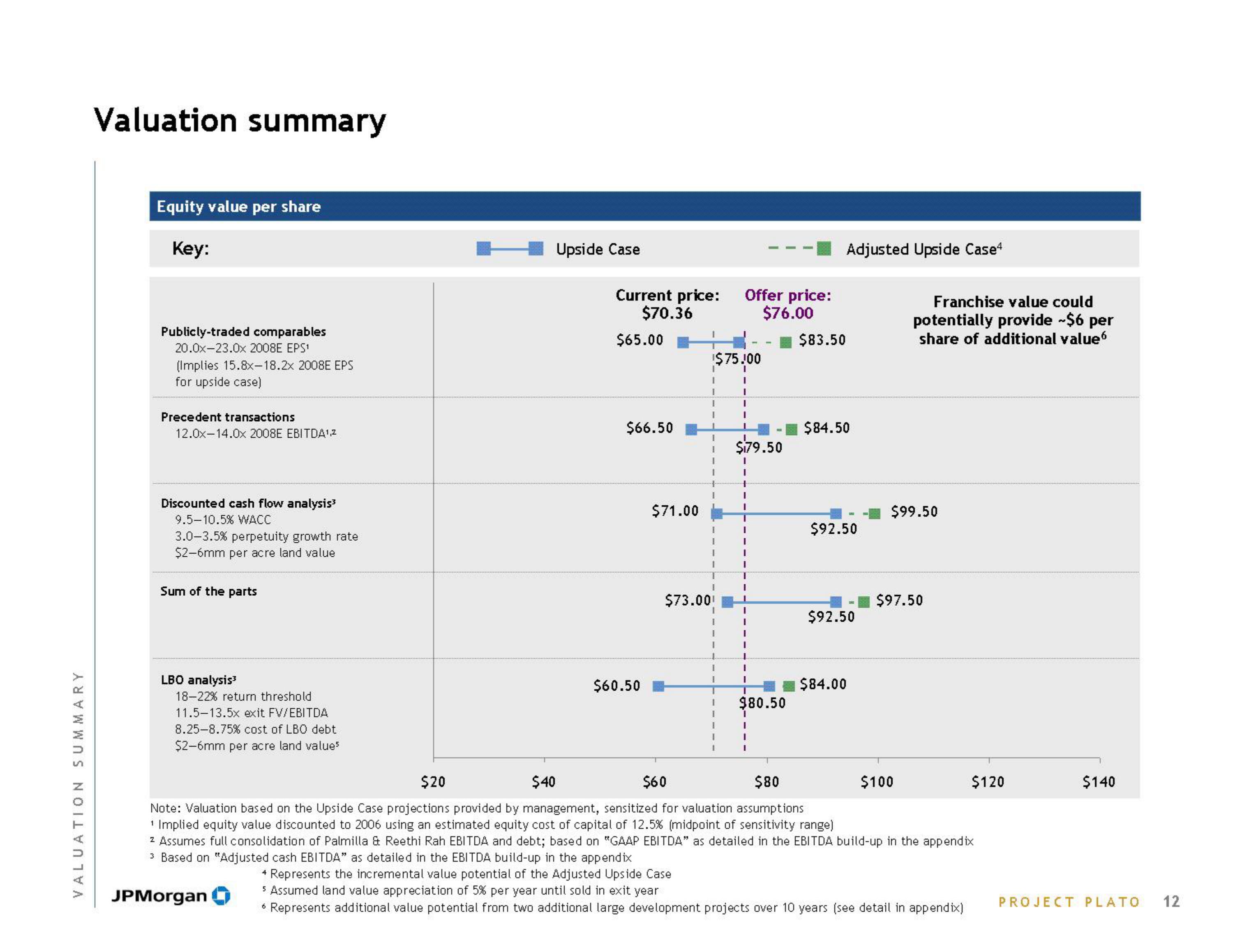

Valuation summary

Equity value per share

Key:

Publicly-traded comparables

20.0x-23.0x 2008E EPS¹

(Implies 15.8x-18.2x 2008E EPS

for upside case)

Precedent transactions

12.0x-14.0x 2008E EBITDA¹,²

Discounted cash flow analysis³

9.5-10.5% WACC

3.0-3.5% perpetuity growth rate

$2-6mm per acre land value

Sum of the parts

LBO analysis³

18-22% return threshold

11.5-13.5x exit FV/EBITDA

8.25-8.75% cost of LBO debt

$2-6mm per acre land values

Upside Case

JPMorgan

Current price:

$70.36

$65.00

$66.50

$60.50

$71.00

I

1

1

$75.00

I

I

1

1

I

I

I

I

I

I

I

$73.00!

I

I

1

Offer price:

$76.00

1

I

I

I

1

T

I

I

I

I

I

$179.50

I

I

H

I

I

1

I

I

I

T

I

I

I

I

I

$80.50

1

I

I

I

$83.50

Adjusted Upside Case4

$84.50

$92.50

$92.50

$84.00

Franchise value could

potentially provide ~$6 per

share of additional value

$99.50

$97.50

$20

$40

$60

$80

Note: Valuation based on the Upside Case projections provided by management, sensitized for valuation assumptions

¹ Implied equity value discounted to 2006 using an estimated equity cost of capital of 12.5 % (midpoint of sensitivity range)

2 Assumes full consolidation of Palmilla & Reethi Rah EBITDA and debt; based on "GAAP EBITDA" as detailed in the EBITDA build-up in the appendix

3 Based on "Adjusted cash EBITDA" as detailed in the EBITDA build-up in the appendix

$100

4 Represents the incremental value potential of the Adjusted Upside Case

5 Assumed land value appreciation of 5% per year until sold in exit year

* Represents additional value potential from two additional large development projects over 10 years (see detail in appendix)

$120

$140

PROJECT PLATO

12View entire presentation