Kinnevik Results Presentation Deck

Intro

Net Asset Value

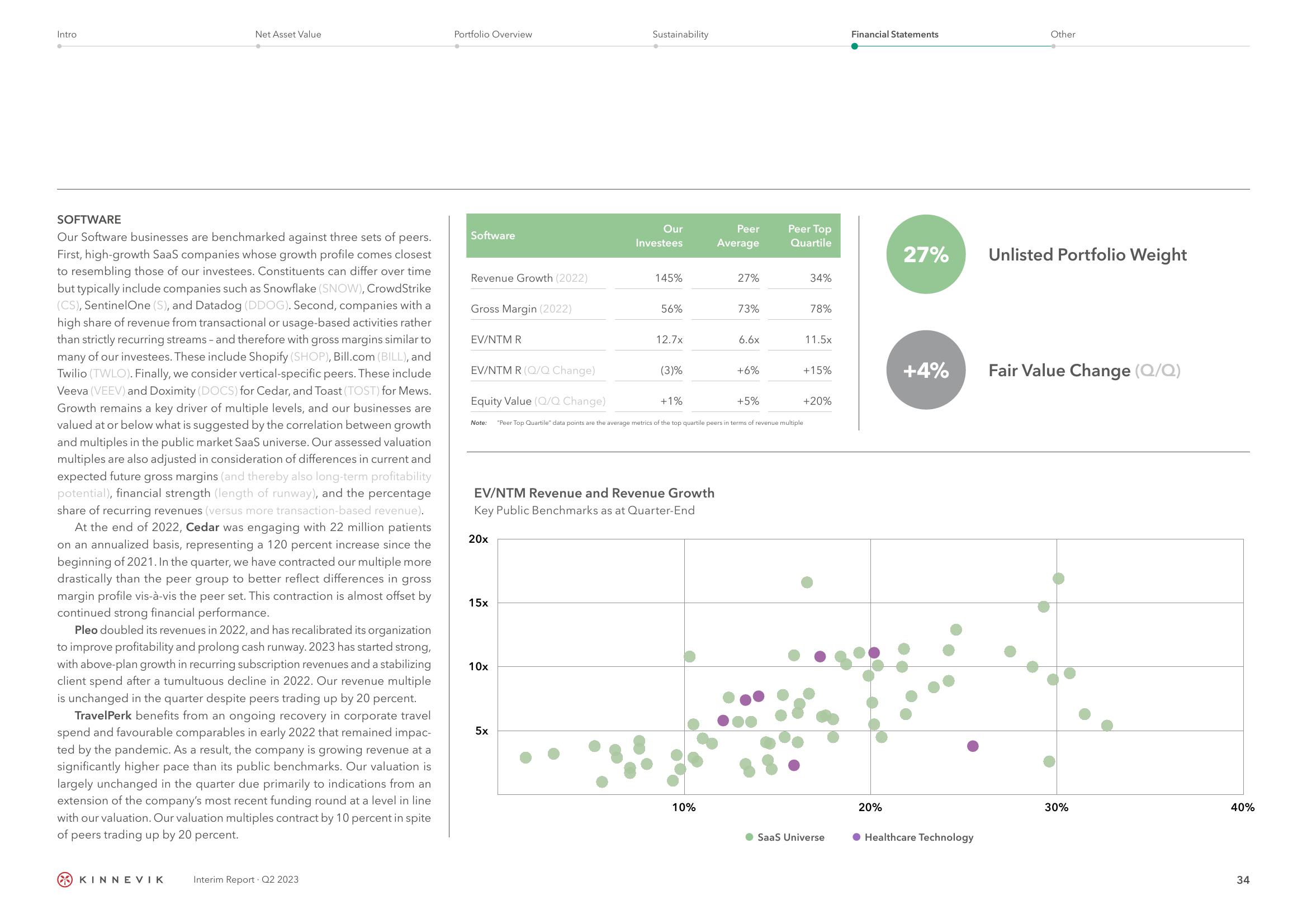

SOFTWARE

Our Software businesses are benchmarked against three sets of peers.

First, high-growth SaaS companies whose growth profile comes closest

to resembling those of our investees. Constituents can differ over time

but typically include companies such as Snowflake (SNOW), CrowdStrike

(CS), SentinelOne (S), and Datadog (DDOG). Second, companies with a

high share of revenue from transactional or usage-based activities rather

than strictly recurring streams - and therefore with gross margins similar to

many of our investees. These include Shopify (SHOP), Bill.com (BILL), and

Twilio (TWLO). Finally, we consider vertical-specific peers. These include

Veeva (VEEV) and Doximity (DOCS) for Cedar, and Toast (TOST) for Mews.

Growth remains a key driver of multiple levels, and our businesses are

valued at or below what is suggested by the correlation between growth

and multiples in the public market SaaS universe. Our assessed valuation

multiples are also adjusted in consideration of differences in current and

expected future gross margins (and thereby also long-term profitability

potential), financial strength (length of runway), and the percentage

share of recurring revenues (versus more transaction-based revenue).

At the end of 2022, Cedar was engaging with 22 million patients

on an annualized basis, representing a 120 percent increase since the

beginning of 2021. In the quarter, we have contracted our multiple more

drastically than the peer group to better reflect differences in gross

margin profile vis-à-vis the peer set. This contraction is almost offset by

continued strong financial performance.

Pleo doubled its revenues in 2022, and has recalibrated its organization

to improve profitability and prolong cash runway. 2023 has started strong,

with above-plan growth in recurring subscription revenues and a stabilizing

client spend after a tumultuous decline in 2022. Our revenue multiple

is unchanged in the quarter despite peers trading up by 20 percent.

TravelPerk benefits from an ongoing recovery in corporate travel

spend and favourable comparables in early 2022 that remained impac-

ted by the pandemic. As a result, the company is growing revenue at a

significantly higher pace than its public benchmarks. Our valuation is

largely unchanged in the quarter due primarily to indications from an

extension of the company's most recent funding round at a level in line

with our valuation. Our valuation multiples contract by 10 percent in spite

of peers trading up by 20 percent.

KINNEVIK

Interim Report Q2 2023

Portfolio Overview

Software

Revenue Growth (2022)

Gross Margin (2022)

EV/NTM R

EV/NTM R (Q/Q Change)

Equity Value (Q/Q Change)

Note:

20x

15x

10x

Sustainability

5x

Our

Investees

145%

56%

12.7x

EV/NTM Revenue and Revenue Growth

Key Public Benchmarks as at Quarter-End

(3)%

+1%

Peer

Average

10%

27%

73%

6.6x

+6%

+5%

Peer Top

Quartile

"Peer Top Quartile" data points are the average metrics of the top quartile peers in terms of revenue multiple

34%

78%

11.5x

+15%

+20%

SaaS Universe

Financial Statements

20%

27%

+4%

Healthcare Technology

Other

Unlisted Portfolio Weight

Fair Value Change (Q/Q)

30%

40%

34View entire presentation