Ford Investor Conference

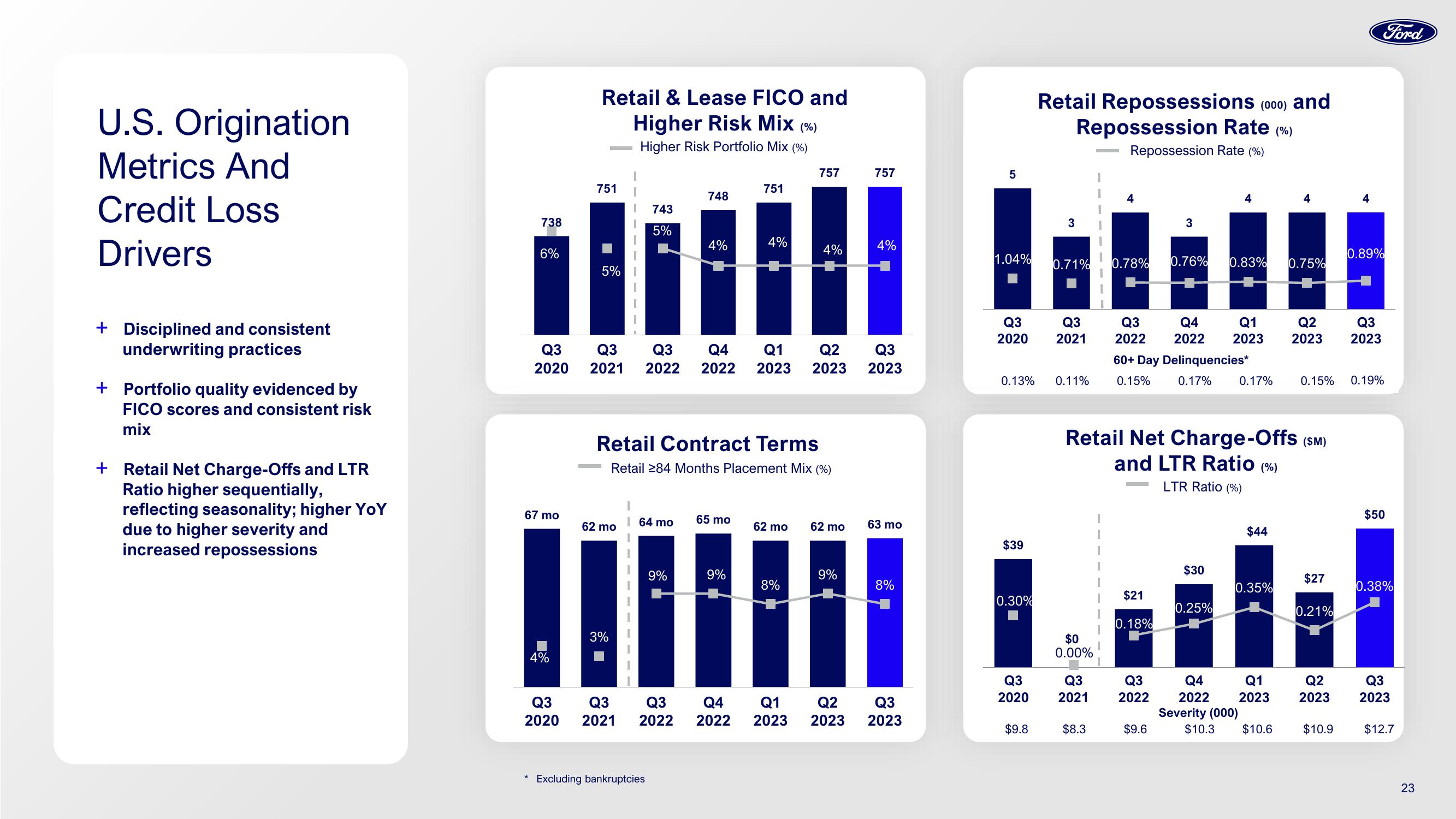

U.S. Origination

Metrics And

Credit Loss

Drivers

+ Disciplined and consistent

underwriting practices

+ Portfolio quality evidenced by

FICO scores and consistent risk

mix

+ Retail Net Charge-Offs and LTR

Ratio higher sequentially,

reflecting seasonality; higher YoY

due to higher severity and

increased repossessions

738

6%

*

Q3

2020

67 mo

4%

Q3

2020

Retail & Lease FICO and

Higher Risk Mix (%)

Higher Risk Portfolio Mix (%)

751

5%

62 mo

743

5%

3%

I

164 mo

Excluding bankruptcies

748

9%

Q3

2021 2022

4%

Q3 Q3 Q4

2021 2022 2022 2023 2023

Retail Contract Terms

Retail 284 Months Placement Mix (%)

751

65 mo

4%

9%

757

4%

Q1 Q2 Q3

2023

8%

62 mo 62 mo

757

9%

4%

63 mo

8%

Q4

Q

Q3

2022 2023 2023 2023

5

1.04%

Q3

2020

0.13%

$39

0.30%

Q3

2020

$9.8

Retail Repossessions (000) and

Repossession Rate (%)

Repossession Rate (%)

3 I

0.71%

Q3

2021

0.11%

$0

0.00%

Q3

2021

$8.3

4

I

0.78%

3

$21

0.18%

Q3 Q4 Q1

2022 2022 2023

60+ Day Delinquencies*

0.15% 0.17%

Retail Net Charge-Offs (SM)

and LTR Ratio (%)

LTR Ratio (%)

$9.6

4

0.76% 0.83% 0.75%

$30

0.25%

0.17%

$44

0.35%

Q3

Q4

2022 2022

Severity (000)

$10.3 $10.6

4

Q1

2023

Q2 Q3

2023 2023

0.15% 0.19%

$27

0.21%

4

Q2

2023

0.89%

$10.9

Ford

$50

0.38%

Q3

2023

$12.7

23View entire presentation