J.P.Morgan Investment Banking Pitch Book

APPENDIX

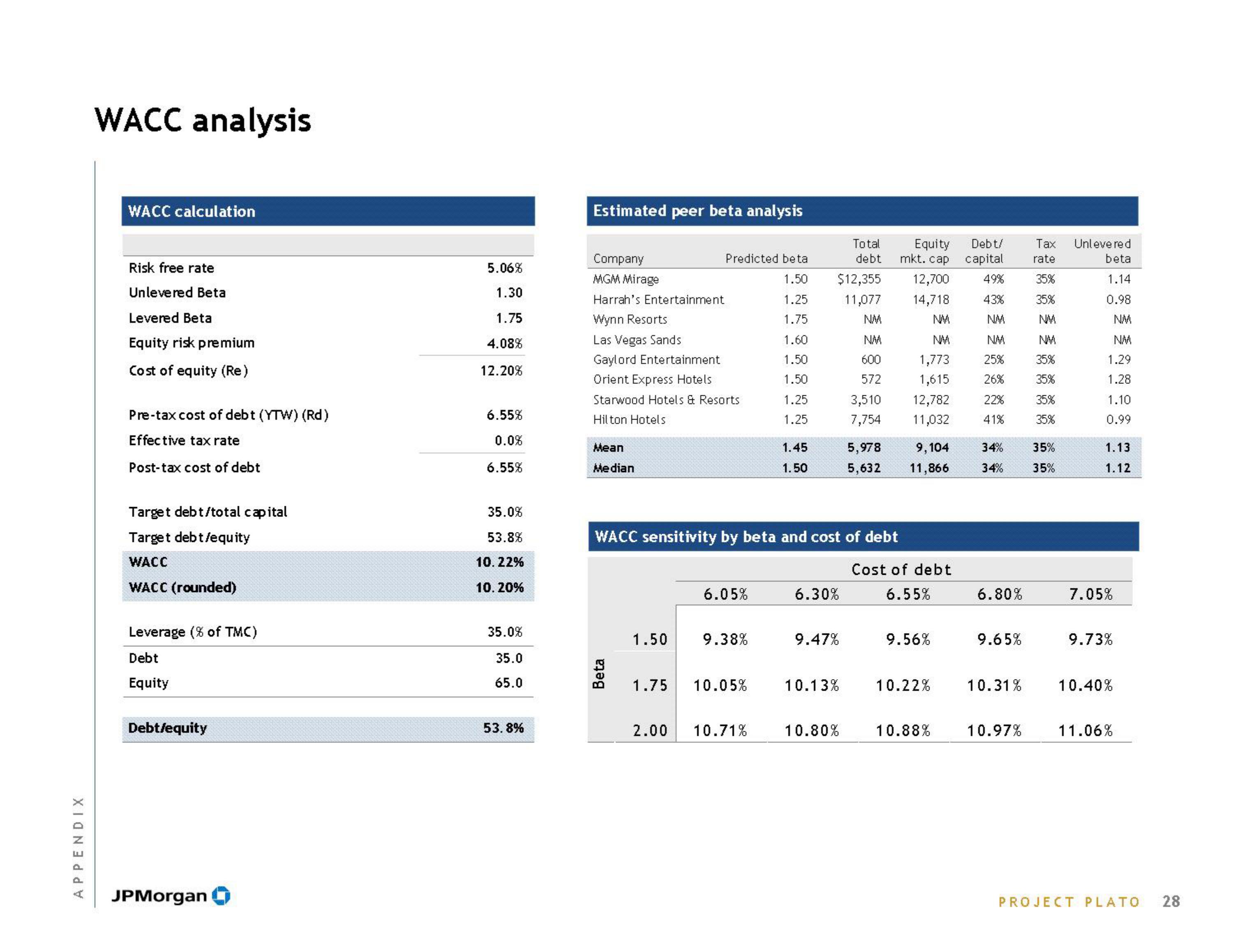

WACC analysis

WACC calculation

Risk free rate

Unlevered Beta

Levered Beta

Equity risk premium

Cost of equity (Re)

Pre-tax cost of debt (YTW) (Rd)

Effective tax rate

Post-tax cost of debt

Target debt/total capital

Target debt/equity

WACC

WACC (rounded)

Leverage (% of TMC)

Debt

Equity

Debt/equity

JPMorgan

5.06%

1.30

1.75

4.08%

12.20%

6.55%

0.0%

6.55%

35.0%

53.8%

10.22%

10.20%

35.0%

35.0

65.0

53.8%

Estimated peer

Mean

Median

Company

MGM Mirage

Harrah's Entertainment

Wynn Resorts

Las Vegas Sands

Gaylord Entertainment

Orient Express Hotels

Starwood Hotels & Resorts

Hilton Hotels

Beta

1.50

beta analysis

1.75

Predicted beta

1.50

1.25

1.75

1.60

1.50

1.50

1.25

1.25

2.00

WACC sensitivity by beta and cost of debt

6.05%

9.38%

10.05%

1.45

1.50

10.71%

Total

debt

$12,355

11,077

NM

6.30%

9.47%

10.13%

NM

600

572

3,510

7,754

5,978

5,632

10.80%

Equity

Debt/

mkt. cap capital

12,700 49%

14,718 43%

NM

NM

NM

NM

25%

26%

1,773

1,615

12,782

11,032

9,104

11,866 34%

22%

41%

34%

Cost of debt

6.55%

9.56%

10.22%

6.80%

9.65%

10.31%

Tax Unlevered

rate

beta

1.14

35%

35%

0.98

NM

NM

NM

1.29

1.28

1.10

0.99

NM

35%

35%

35%

35%

35%

35%

1.13

1.12

7.05%

9.73%

10.40%

10.88% 10.97% 11.06%

PROJECT PLATO

28View entire presentation