Paysafe Results Presentation Deck

Strong balance sheet - Debt restructuring enhances financial flexibility

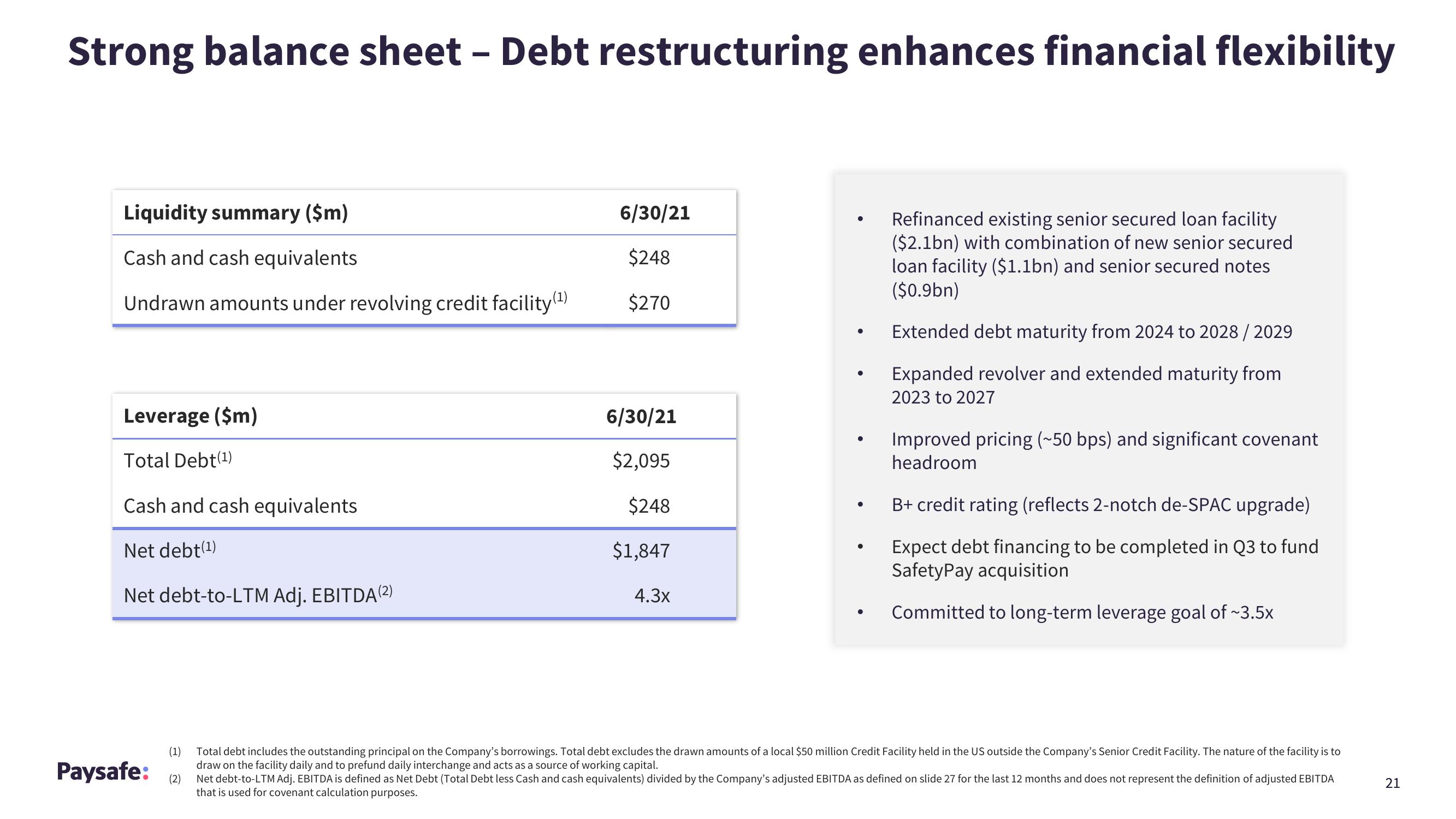

Liquidity summary ($m)

Cash and cash equivalents

Undrawn amounts under revolving credit facility (¹)

Leverage ($m)

Total Debt(¹)

Cash and cash equivalents

Net debt(¹)

Net debt-to-LTM Adj. EBITDA(2)

Paysafe:

(1)

(2)

6/30/21

$248

$270

6/30/21

$2,095

$248

$1,847

4.3x

●

●

Refinanced existing senior secured loan facility

($2.1bn) with combination of new senior secured

loan facility ($1.1bn) and senior secured notes

($0.9bn)

Extended debt maturity from 2024 to 2028 / 2029

Expanded revolver and extended maturity from

2023 to 2027

Improved pricing (~50 bps) and significant covenant

headroom

B+ credit rating (reflects 2-notch de-SPAC upgrade)

Expect debt financing to be completed in Q3 to fund

SafetyPay acquisition

Committed to long-term leverage goal of ~3.5x

Total debt includes the outstanding principal on the Company's borrowings. Total debt excludes the drawn amounts of a local $50 million Credit Facility held in the US outside the Company's Senior Credit Facility. The nature of the facility is to

draw on the facility daily and to prefund daily interchange and acts as a source of working capital.

Net debt-to-LTM Adj. EBITDA is defined as Net Debt (Total Debt less Cash and cash equivalents) divided by the Company's adjusted EBITDA as defined on slide 27 for the last 12 months and does not represent the definition of adjusted EBITDA

that is used for covenant calculation purposes.

21View entire presentation