Inovalon Results Presentation Deck

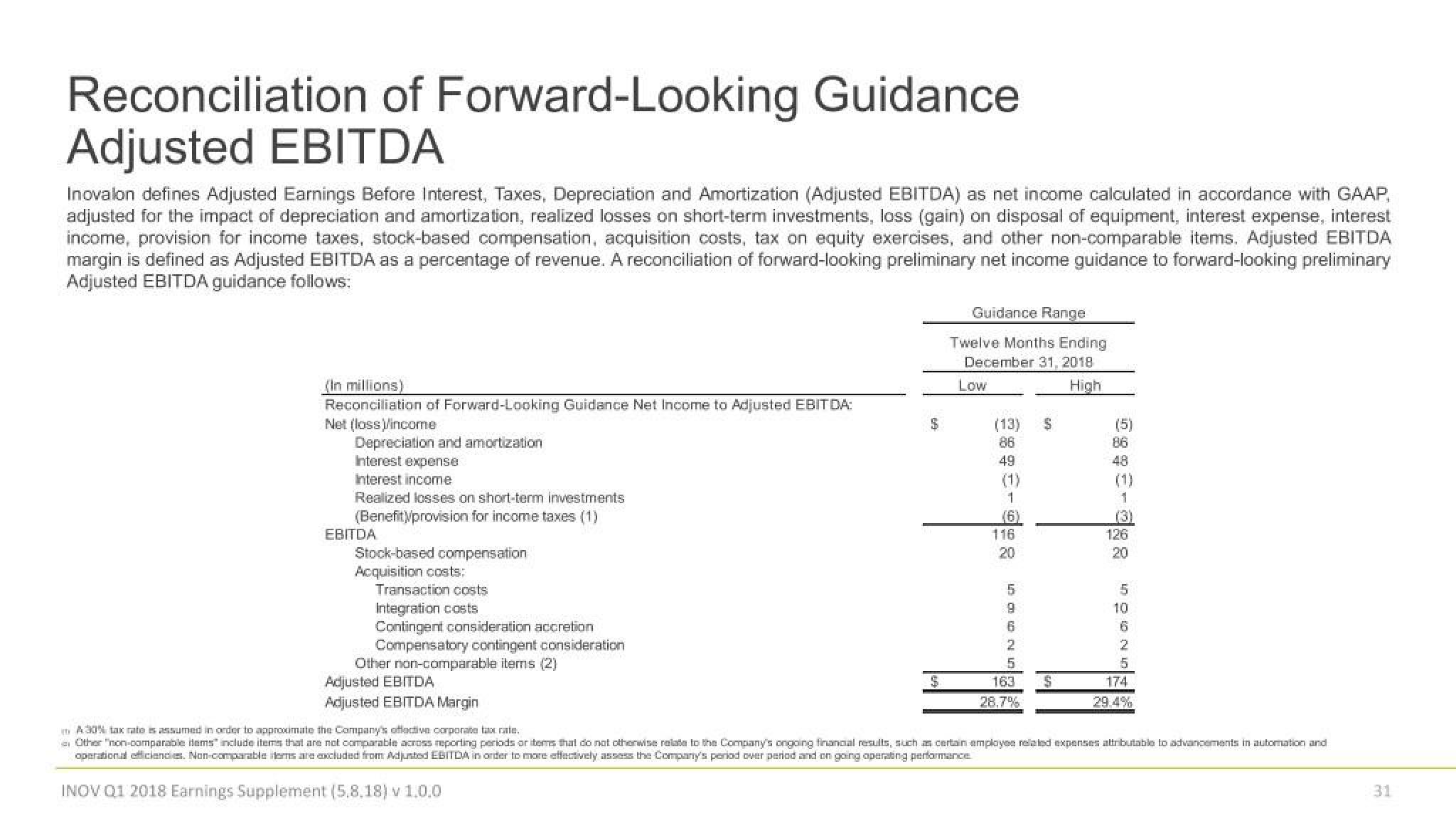

Reconciliation of Forward-Looking Guidance

Adjusted EBITDA

Inovalon defines Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (Adjusted EBITDA) as net income calculated in accordance with GAAP,

adjusted for the impact of depreciation and amortization, realized losses on short-term investments, loss (gain) on disposal of equipment, interest expense, interest

income, provision for income taxes, stock-based compensation, acquisition costs, tax on equity exercises, and other non-comparable items. Adjusted EBITDA

margin is defined as Adjusted EBITDA as a percentage of revenue. A reconciliation of forward-looking preliminary net income guidance to forward-looking preliminary

Adjusted EBITDA guidance follows:

(In millions)

Reconciliation of Forward-Looking Guidance Net Income to Adjusted EBITDA:

Net (loss)/income

Depreciation and amortization

Interest expense

Interest income

Realized losses on short-term investments

(Benefit)//provision for income taxes (1)

EBITDA

Stock-based compensation

Acquisition costs:

Transaction costs

Integration costs

Contingent consideration accretion

Compensatory contingent consideration

Other non-comparable items (2)

Adjusted EBITDA

Adjusted EBITDA Margin

$

$

Guidance Range

Twelve Months Ending

December 31, 2018

High

Low

86

49

(1)

1

(6)

116

20

5

9

6

2

5

163

28,7%

$

S

(5)

86

(1)

+

(3)

126

20

5

10

5

174

29.4%

m A 30% tax rate is assumed in order to approximate the Company's offective corporate tax rate.

Other "non-comparable items include items that are not comparable across reporting periods or items that do not otherwise relate to the Company's ongoing financial results, such as certain employee related expenses attributable to advancements in automation and

operational efficiencies. Non-comparable items are excluded from Adjusted EBITDA in order to more effectively assess the Company's period over period and on going operating performance.

INOV Q1 2018 Earnings Supplement (5,8,18) v 1.0.0

31View entire presentation