Oatly Results Presentation Deck

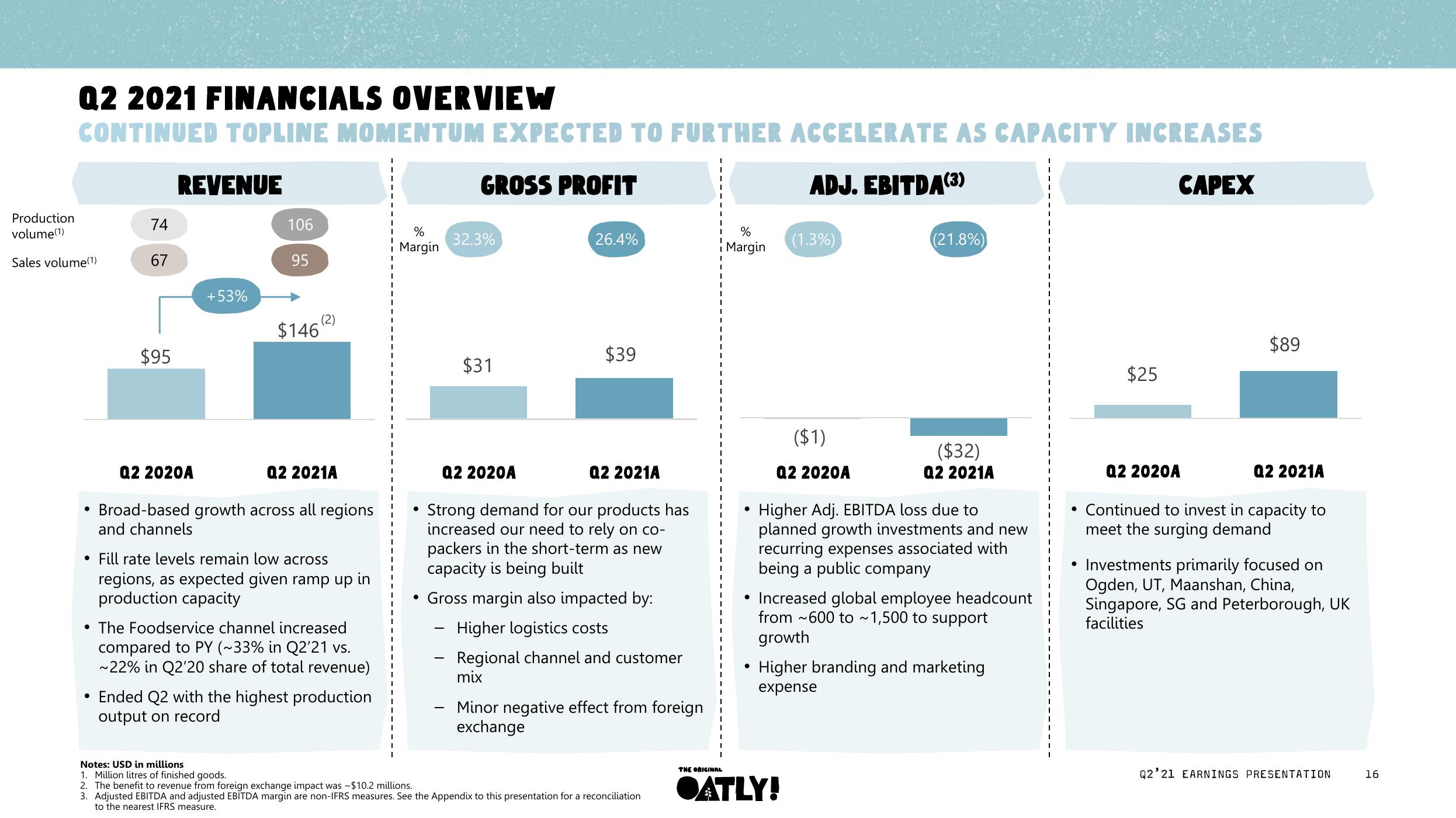

Q2 2021 FINANCIALS OVERVIEW

CONTINUED TOPLINE MOMENTUM EXPECTED TO FURTHER ACCELERATE AS CAPACITY INCREASES

ADJ. EBITDA (3)

CAPEX

Production

volume (1)

Sales volume(1)

●

●

74

67

●

$95

REVENUE

+53%

Q2 2020A

106

95

$146

Q2 2021A

Broad-based growth across all regions

and channels

• Fill rate levels remain low across

regions, as expected given ramp up in

production capacity

The Foodservice channel increased

compared to PY (~33% in Q2'21 vs.

~22% in Q2'20 share of total revenue)

Ended Q2 with the highest production

output on record

%

Margin

●

●

-

-

GROSS PROFIT

-

32.3%

$31

Q2 2020A

Strong demand for our products has

increased our need to rely on co-

packers in the short-term as new

capacity is being built

Gross margin also impacted by:

Higher logistics costs

26.4%

$39

Q2 2021A

Regional channel and customer

mix

Minor negative effect from foreign

exchange

Notes: USD in millions

1. Million litres of finished goods.

2. The benefit to revenue from foreign exchange impact was ~$10.2 millions.

3. Adjusted EBITDA and adjusted EBITDA margin are non-IFRS measures. See the Appendix to this presentation for a reconciliation

to the nearest IFRS measure.

THE ORIGINAL

%

Margin

●

(1.3%)

(21.8%)

($1)

Q2 2020A

Higher Adj. EBITDA loss due to

planned growth investments and new

recurring expenses associated with

being a public company

●ATLY!

($32)

Q2 2021A

• Increased global employee headcount

from ~600 to ~1,500 to support

growth

Higher branding and marketing

expense

$25

$89

Q2 2021A

Q2 2020A

• Continued to invest in capacity to

meet the surging demand

• Investments primarily focused on

Ogden, UT, Maanshan, China,

Singapore, SG and Peterborough, UK

facilities

Q2'21 EARNINGS PRESENTATION

16View entire presentation