Antero Midstream Partners Investor Presentation Deck

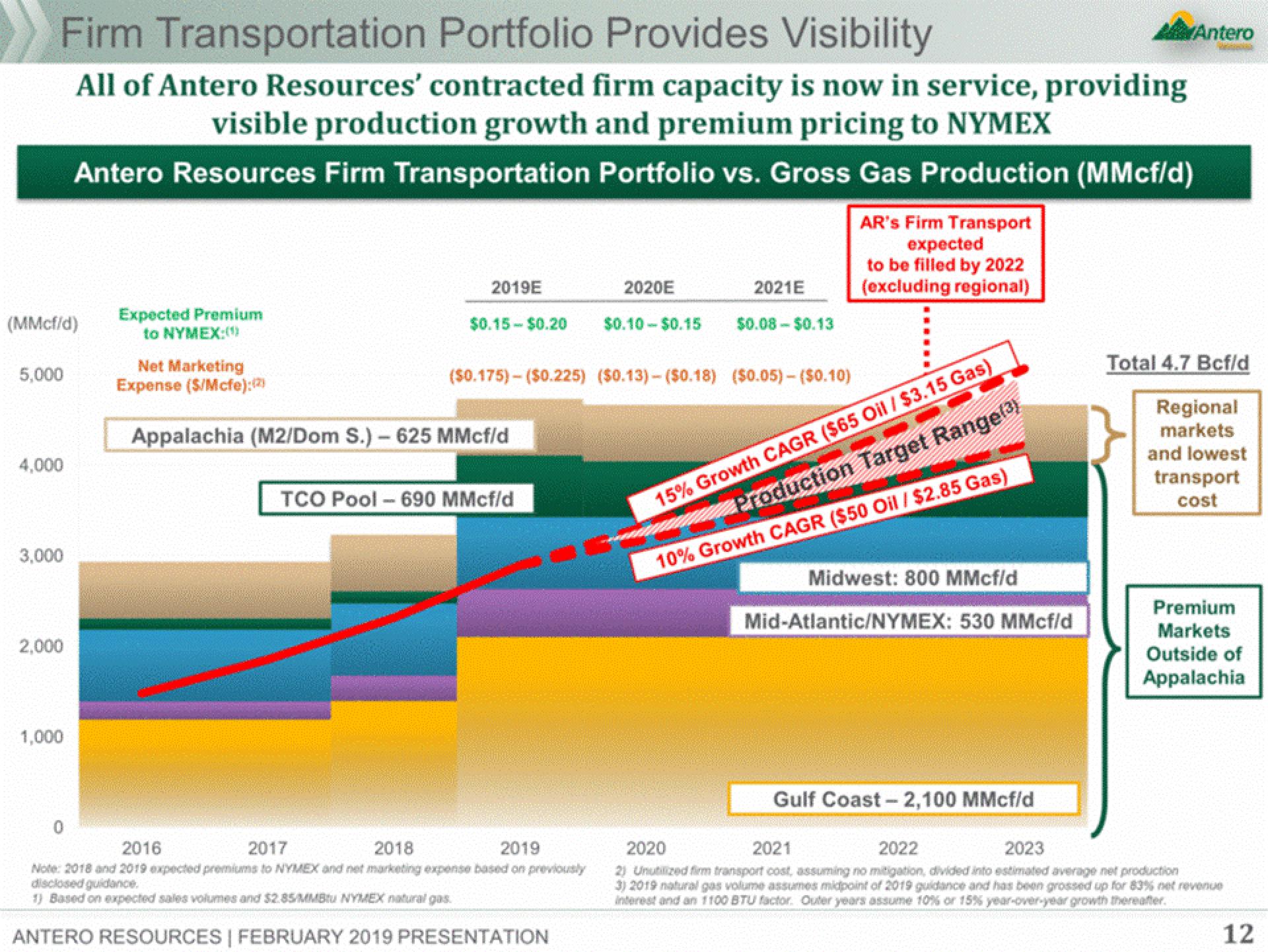

Firm Transportation Portfolio Provides Visibility

All of Antero Resources' contracted firm capacity is now in service, providing

visible production growth and premium pricing to NYMEX

Antero Resources Firm Transportation Portfolio vs. Gross Gas Production (MMcf/d)

(MMcf/d)

5,000

4,000

3,000

2,000

1,000

0

Expected Premium

to NYMEX:(¹)

Net Marketing

Expense ($/Mcfe):(2)

2019E

2020E

$0.15-$0.20 $0.10-$0.15

($0.175)-($0.225) ($0.13)-($0.18) ($0.05)-($0.10)

Appalachia (M2/Dom S.)- 625 MMcf/d

TCO Pool - 690 MMcf/d

2016

2017

2018

2019

Note: 2018 and 2019 expected premiums to NYMEX and net marketing expense based on previously

disclosed guidance.

1) Based on expected sales volumes and $2.85/MMB NYMEX natural gas

2021E

$0.08-$0.13

ANTERO RESOURCES | FEBRUARY 2019 PRESENTATION

AR's Firm Transport

expected

to be filled by 2022

(excluding regional)

15% Growth CAGR ($65 Oil / $3.15 Gas)

Production Target Range(³)

10% Growth CAGR ($50 Oil / $2.85 Gas)

Midwest: 800 MMcf/d

Mid-Atlantic/NYMEX: 530 MMcf/d

Gulf Coast - 2,100 MMcf/d

Antero

Total 4.7 Bcf/d

Regional

markets

and lowest

transport

cost

Premium

Markets

Outside of

Appalachia

2020

2021

2022

2023

2) Unutilized firm transport cost, assuming no mitigation, divided into estimated average net production

3) 2019 natural gas volume assumes midpoint of 2019 guidance and has been grossed up for 83% net revenue

Interest and on 1100 BTU factor. Outer years assume 10% or 15% year-over-year growth thereafter.

12View entire presentation