Inovalon Results Presentation Deck

Reconciliation

Non-GAAP Net Income

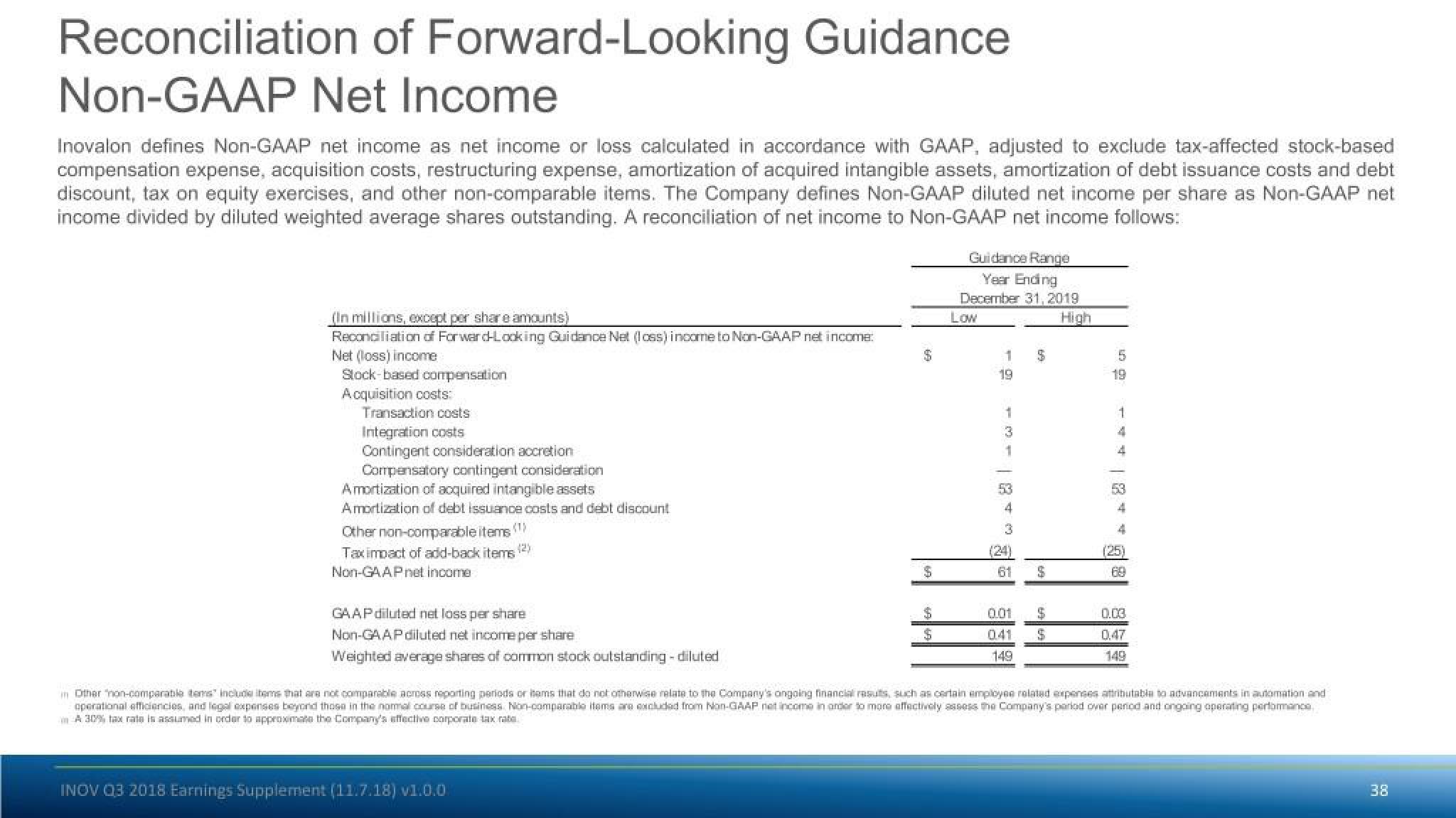

Inovalon defines Non-GAAP net income as net income or loss calculated in accordance with GAAP, adjusted to exclude tax-affected stock-based

compensation expense, acquisition costs, restructuring expense, amortization of acquired intangible assets, amortization of debt issuance costs and debt

discount, tax on equity exercises, and other non-comparable items. The Company defines Non-GAAP diluted net income per share as Non-GAAP net

income divided by diluted weighted average shares outstanding. A reconciliation of net income to Non-GAAP net income follows:

of Forward-Looking Guidance

(In millions, except per share amounts)

Reconciliation of Forward-Looking Guidance Net (loss) income to Non-GAAP net income:

Net (loss) income

Stock-based compensation

Acquisition costs:

Transaction costs

Integration costs

Contingent consideration accretion

Compensatory contingent consideration

Amortization of acquired intangible assets

Amortization of debt issuance costs and debt discount

Other non-comparable items (¹)

Taximpact of add-back items (2)

Non-GAAP net income

GAAP diluted net loss per share

Non-GAAP diluted net income per share

Weighted average shares of common stock outstanding-diluted

69

INOV Q3 2018 Earnings Supplement (11.7.18) v1.0.0

$

$

$

Guidance Range

Year Ending

December 31, 2019

Low

1 $

19

هان |

53

(24)

61

041

149

$

$

S

High

5

tr

19

1

4

** 8*

4

4

25)

69

0.03

149

in Other non-comparable items include items that are not comparable across reporting periods or items that do not otherwise relate to the Company's ongoing financial results, such as certain employee related expenses attributable to advancements in automation and

operational efficiencies, and legal expenses beyond those in the normal course of business Non-comparable items are excluded from Non-GAAP net income in order to more effectively assess the Company's parlod over period and ongoing operating performance

A 30% tax rate is assumed in order to approximate the Company's effective corporate tax rate

38View entire presentation