J.P.Morgan Results Presentation Deck

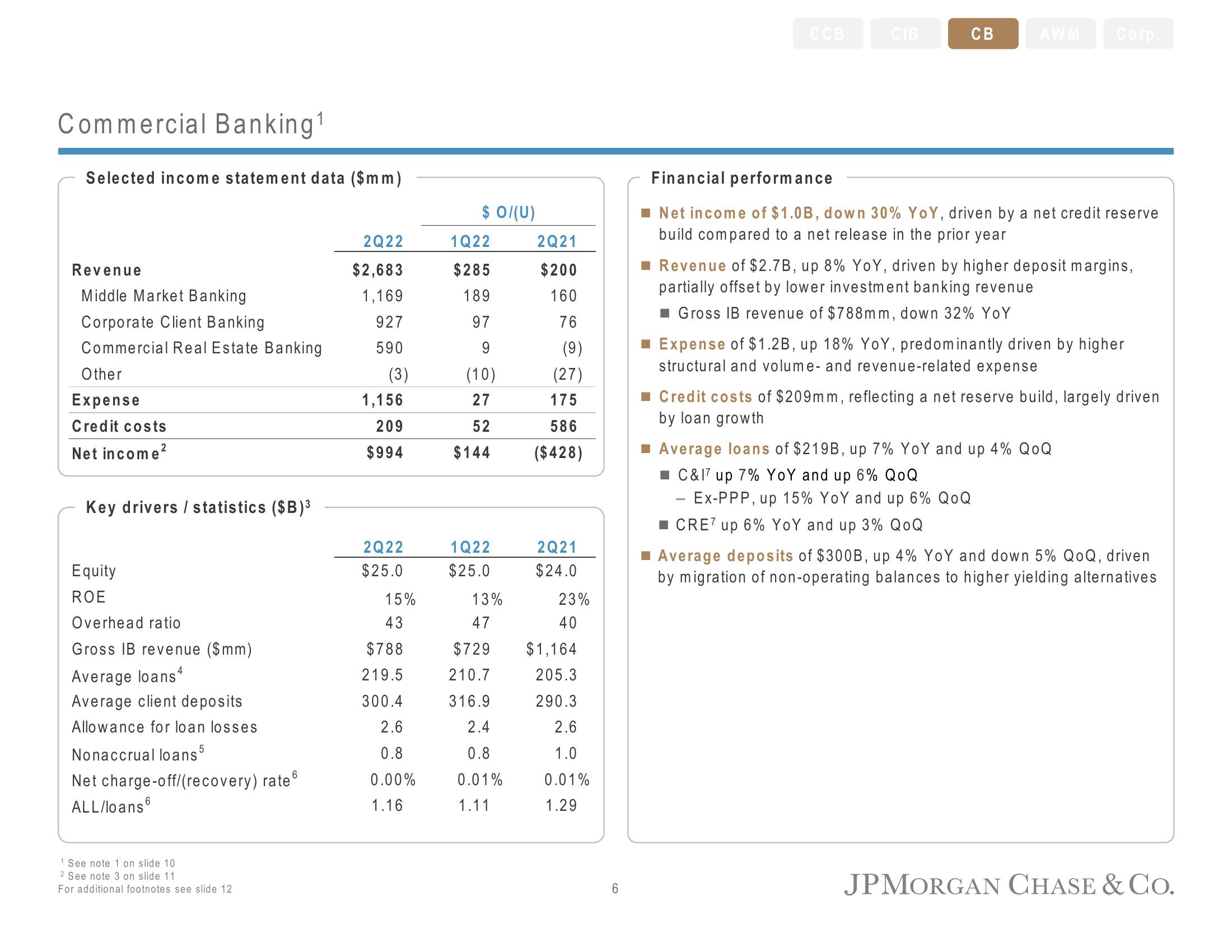

Commercial Banking¹

Selected income statement data ($mm)

Revenue

Middle Market Banking

Corporate Client Banking

Commercial Real Estate Banking

Other

Expense

Credit costs

Net income²

Key drivers / statistics ($B)³

Equity

ROE

Overhead ratio

Gross IB revenue ($mm)

Average loans4

Average client deposits

Allowance for loan losses

Nonaccrual loans 5

6

Net charge-off/(recovery) rate

ALL/loans

1 See note 1 on slide 10

2 See note 3 on slide 11.

For additional footnotes see slide 12

2Q22

$2,683

1,169

927

590

(3)

1,156

209

$994

2Q22

$25.0

15%

43

$788

219.5

300.4

2.6

0.8

0.00%

1.16

$ 0/(U)

1Q22

$285

189

97

(10)

27

52

$144

1Q22

$25.0

13%

47

$729

210.7

316.9

2.4

0.8

0.01%

1.11

2Q21

$200

160

76

(9)

(27)

175

586

($428)

2Q21

$24.0

23%

40

$1,164

205.3

290.3

2.6

1.0

0.01%

1.29

6

CIB

CB

AWM Corp.

Financial performance

Net income of $1.0B, down 30% YoY, driven by a net credit reserve

build compared to a net release in the prior year

■ Revenue of $2.7B, up 8% YoY, driven by higher deposit margins,

partially offset by lower investment banking revenue

■ Gross IB revenue of $788mm, down 32% YoY

■ Expense of $1.2B, up 18% YoY, predominantly driven by higher

structural and volume- and revenue-related expense

■ Credit costs of $209mm, reflecting a net reserve build, largely driven

by loan growth

■ Average loans of $219B, up 7% YoY and up 4% QOQ

■ C&17 up 7% YoY and up 6% QOQ

- Ex-PPP, up 15% YoY and up 6% QOQ

CRE7 up 6% YoY and up 3% QOQ

■ Average deposits of $300B, up 4% YoY and down 5% QoQ, driven

by migration of non-operating balances to higher yielding alternatives

JPMORGAN CHASE & Co.View entire presentation