Evercore Investment Banking Pitch Book

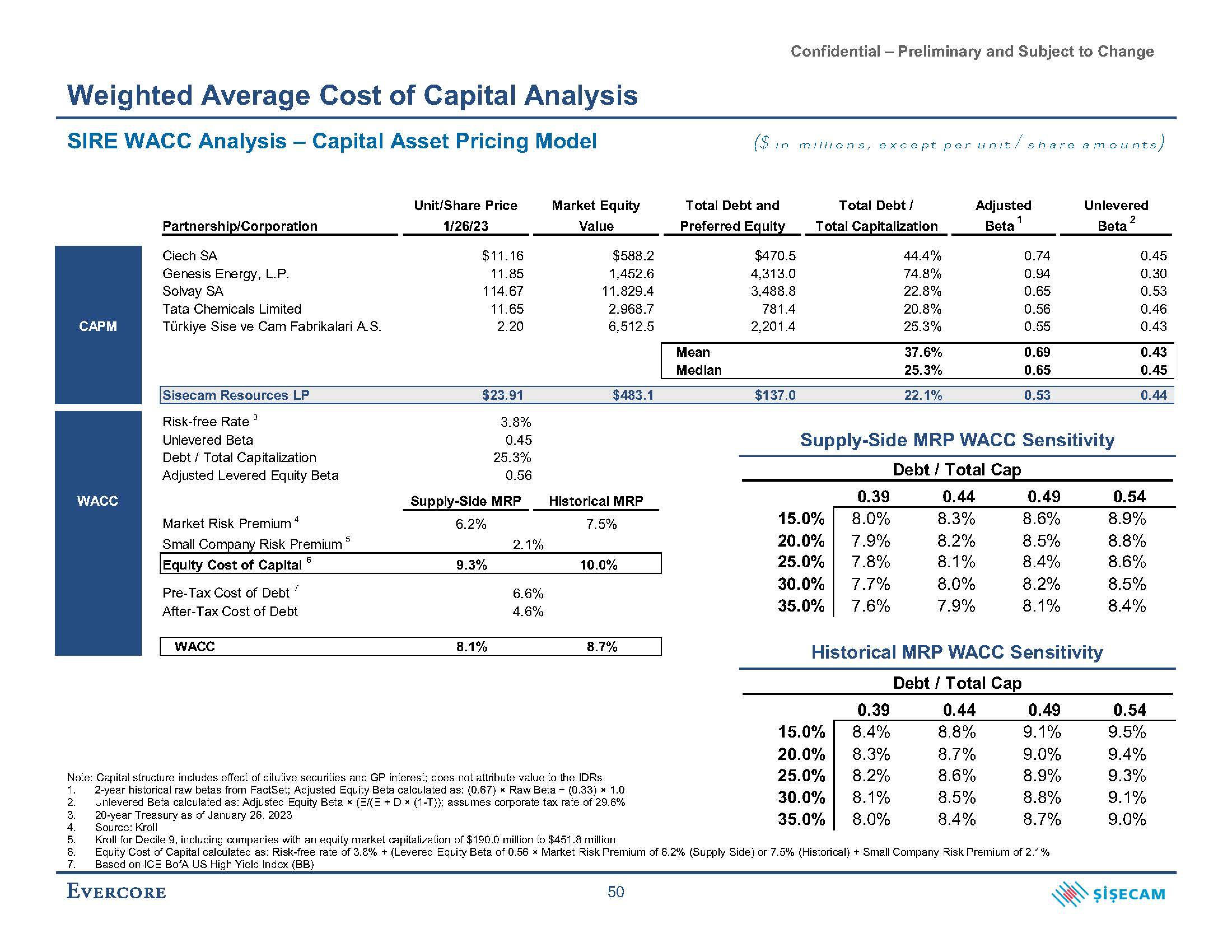

Weighted Average Cost of Capital Analysis

SIRE WACC Analysis - Capital Asset Pricing Model

CAPM

WACC

1.

2.

3.

4.

5.

6.

7.

Partnership/Corporation

Ciech SA

Genesis Energy, L.P.

Solvay SA

Tata Chemicals Limited

Türkiye Sise ve Cam Fabrikalari A.S.

Sisecam Resources LP

3

Risk-free Rate

Unlevered Beta

Debt Total Capitalization

Adjusted Levered Equity Beta

4

Market Risk Premium

Small Company Risk Premium

6

Equity Cost of Capital

Pre-Tax Cost of Debt?

After-Tax Cost of Debt

WACC

5

Unit/Share Price

1/26/23

$11.16

11.85

114.67

11.65

2.20

$23.91

3.8%

0.45

25.3%

0.56

Supply-Side MRP

6.2%

9.3%

8.1%

2.1%

6.6%

4.6%

Market Equity

Value

$588.2

1,452.6

11,829.4

2,968.7

6,512.5

$483.1

Historical MRP

7.5%

10.0%

8.7%

Note: Capital structure includes effect of dilutive securities and GP interest; does not attribute value to the IDRs

2-year historical raw betas from FactSet; Adjusted Equity Beta calculated as: (0.67) * Raw Beta + (0.33) × 1.0

Unlevered Beta calculated as: Adjusted Equity Beta x (E/(E + D x (1-T)); assumes corporate tax rate of 29.6%

20-year Treasury as of January 26, 2023

Source: Kroll

50

Total Debt and

Preferred Equity

Mean

Median

Confidential - Preliminary and Subject to Change

($ in millions, except per unit/ share amounts,

$470.5

4,313.0

3,488.8

781.4

2,201.4

$137.0

Total Debt /

Total Capitalization

0.39

15.0% 8.0%

20.0% 7.9%

25.0% 7.8%

30.0%

7.7%

35.0% 7.6%

44.4%

74.8%

22.8%

20.8%

25.3%

37.6%

25.3%

22.1%

0.39

15.0% 8.4%

20.0% 8.3%

25.0% 8.2%

30.0% 8.1%

35.0% 8.0%

Adjusted

Beta

1

Supply-Side MRP WACC Sensitivity

Debt / Total Cap

0.44

8.3%

8.2%

8.1%

0.74

0.94

0.65

0.56

0.55

8.0%

7.9%

0.69

0.65

0.53

0.49

8.6%

8.5%

8.4%

8.2%

8.1%

Historical MRP WACC Sensitivity

Debt / Total Cap

0.44

8.8%

8.7%

8.6%

8.5%

8.4%

Unlevered

Beta

2

0.49

9.1%

9.0%

8.9%

8.8%

8.7%

Kroll for Decile 9, including companies with an equity market capitalization of $190.0 million to $451.8 million

Equity Cost of Capital calculated as: Risk-free rate of 3.8% + (Levered Equity Beta of 0.56 x Market Risk Premium of 6.2% (Supply Side) or 7.5% (Historical) + Small Company Risk Premium of 2.1%

Based on ICE BofA US High Yield Index (BB)

EVERCORE

0.45

0.30

0.53

0.46

0.43

0.43

0.45

0.44

0.54

8.9%

8.8%

8.6%

8.5%

8.4%

0.54

9.5%

9.4%

9.3%

9.1%

9.0%

ŞİŞECAMView entire presentation