Evercore Investment Banking Pitch Book

Appendix

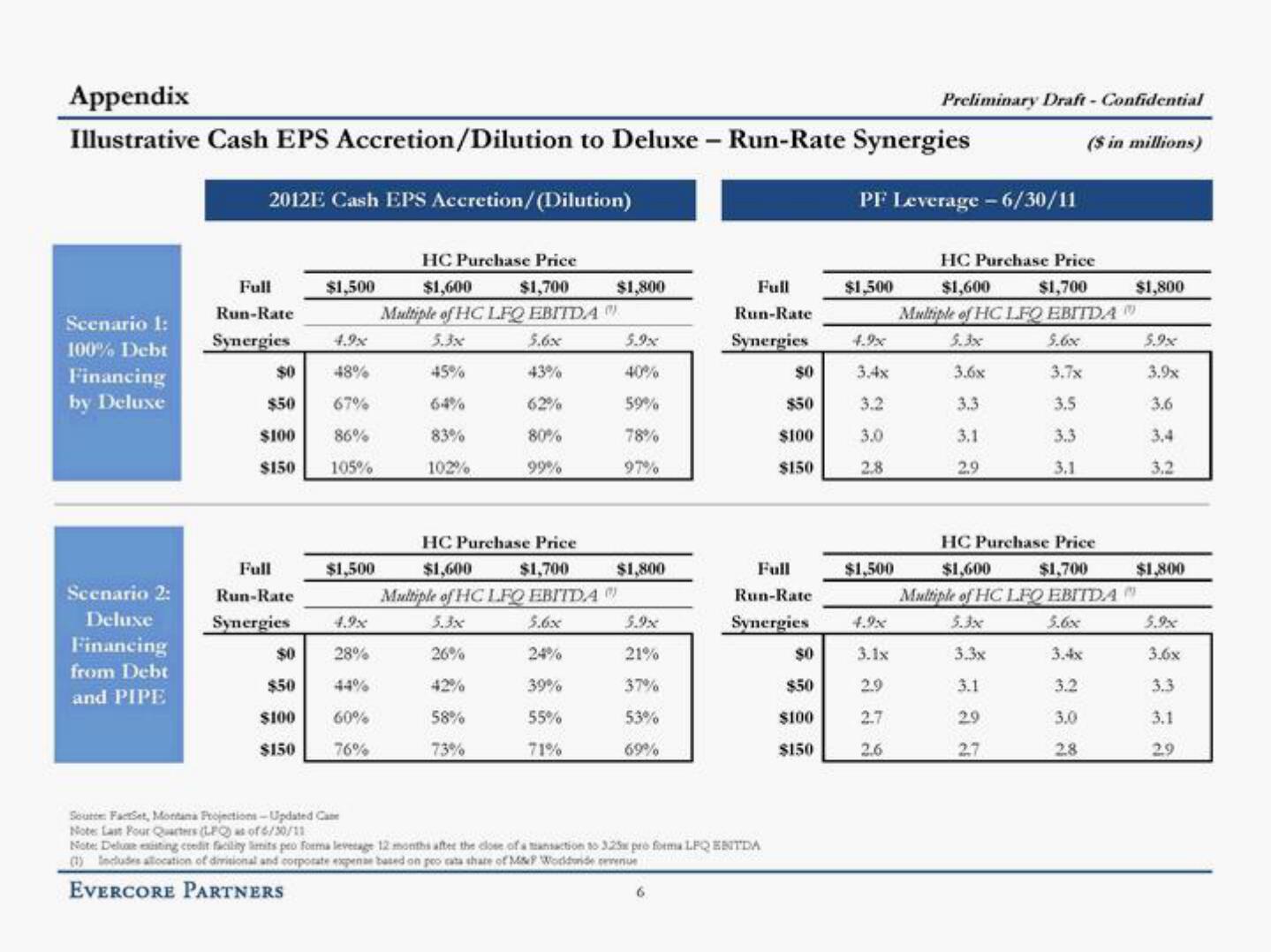

Illustrative Cash EPS Accretion/Dilution to Deluxe - Run-Rate Synergies

2012E Cash EPS Accretion/(Dilution)

Scenario 1:

100% Debt

Financing

by Deluxe

Scenario 2:

Deluxe

Financing

from Debt

and PIPE

Full

Run-Rate

Synergies

$0

$50

$100

$150

Full

Run-Rate

Synergies

$0

$50

$100

$150

$1,500

4.9x

48%

67%

86%

105%

$1,500

4.9x

28%

44%

60%

76%

HC Purchase Price

$1,600

$1,700

Multiple of HC LFQ EBITDA)

5.3x

5.6x

45%

43%

64%

62%

83%

80%

102%

99%

HC Purchase Price

$1,600 $1,700

Multiple of HC LFQ EBITDA)

5.3x

26%

58%

73%

5.6x

$1,800

39%

55%

71%

5.9%

40%

59%

78%

97%

$1,800

5.9x

21%

37%

53%

69%

Full

Run-Rate

Synergies

6

Soutte FactSet, Montana Projections-Updated Cate

Note Last Four Quarters (LPQ) as of 6/30/11

Note: Deluxe existing credit facility limits peo forma leverage 12 months after the close of a transaction to 3.25 pro forma LFQ EBITDA

(1) Includes allocation of divisional and corporate expense based on peo cata share of MS Wordonde enue

EVERCORE PARTNERS

$0

$50

$100

$150

Full

Run-Rate

Synergies

$0

$50

$100

$150

PF Leverage-6/30/11

$1,500

4.9%

3.4x

3.2

3.0

2.8

$1,500

4.9x

3.1x

2.9

Preliminary Draft - Confidential

($ in millions)

2.7

2.6

HC Purchase Price

$1,700

$1,600

Multiple of HC LFQ EBITDA

5.3%

5.6x

3.7x

3.5

3.3

3.1

3.6x

3.3

3.1

2.9

HC Purchase Price

$1,600 $1,700

Multiple of HC LFQ EBITDA

5.3x

5.6x

3.3x

3.1

29

2.7

3.4x

3.2

3.0

28

$1,800

5.9x

3.9x

3.6

3.2

$1,800

5.9%

3.6x

3.3

3.1

29View entire presentation