J.P.Morgan Results Presentation Deck

Commercial Banking1

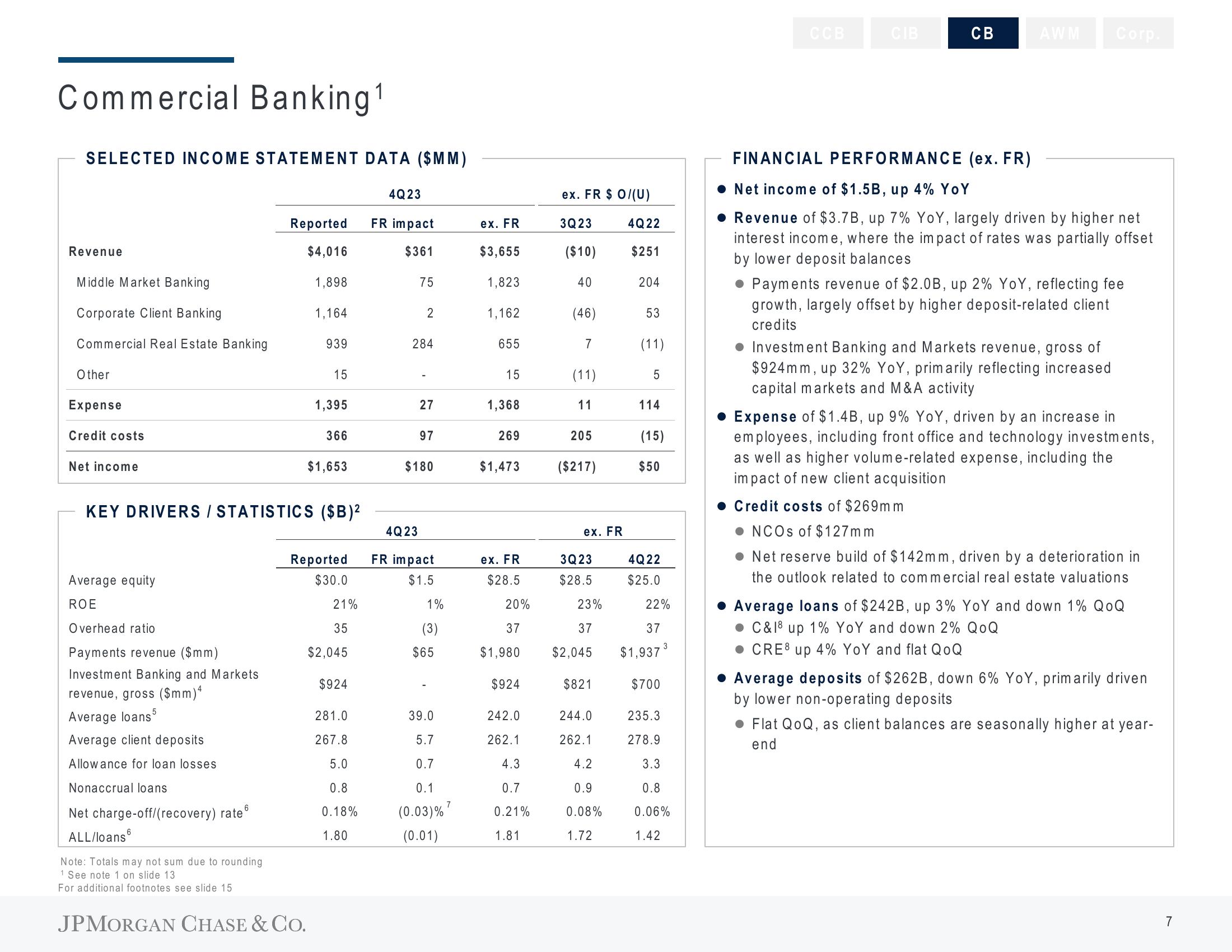

SELECTED INCOME STATEMENT DATA ($MM)

Revenue

Middle Market Banking

Corporate Client Banking

Commercial Real Estate Banking

Other

Expense

Credit costs

Net income

Average equity

ROE

Reported

$4,016

1,898

Overhead ratio

Payments revenue ($mm)

Investment Banking and Markets

revenue, gross ($mm)4

5

Average loans

Average client deposits

Allowance for loan losses

Nonaccrual loans

Net charge-off/(recovery) rate

ALL/loans

Note: Totals may not sum due to rounding

1 See note 1 on slide 13

For additional footnotes see slide 15

1,164

939

JPMORGAN CHASE & CO.

15

1,395

KEY DRIVERS / STATISTICS ($B)²

366

$1,653

Reported

$30.0

21%

35

$2,045

$924

281.0

267.8

5.0

0.8

0.18%

1.80

4Q23

FR impact

$361

75

2

284

4Q23

27

97

$180

FR impact

$1.5

1%

(3)

$65

39.0

5.7

0.7

0.1

(0.03) %

(0.01)

7

ex. FR

$3,655

1,823

1,162

655

15

1,368

269

$1,473

ex. FR

$28.5

20%

37

$1,980

$924

242.0

262.1

4.3

0.7

0.21%

1.81

ex. FR $ 0/(U)

3Q23

($10)

40

(46)

7

(11)

11

205

($217)

ex. FR

3Q23

$28.5

23%

37

$2,045

$821

244.0

262.1

4.2

0.9

0.08%

1.72

4Q22

$251

204

53

(11)

5

114

(15)

$50

4Q22

$25.0

22%

37

$1,937³

$700

235.3

278.9

3.3

0.8

0.06%

1.42

CCB

CIB

CB

AWM Corp.

FINANCIAL PERFORMANCE (ex. FR)

• Net income of $1.5B, up 4% YoY

Revenue of $3.7B, up 7% YoY, largely driven by higher net

interest income, where the impact of rates was partially offset

by lower deposit balances

● Payments revenue of $2.0B, up 2% YoY, reflecting fee

growth, largely offset by higher deposit-related client

credits

Investment Banking and Markets revenue, gross of

$924mm, up 32% YoY, primarily reflecting increased

capital markets and M&A activity

Expense of $1.4B, up 9% YoY, driven by an increase in

employees, including front office and technology investments,

as well as higher volume-related expense, including the

impact of new client acquisition

Credit costs of $269mm

NCOs of $127mm

.Net reserve build of $142mm, driven by a deterioration in

the outlook related to commercial real estate valuations

• Average loans of $242B, up 3% YoY and down 1% QOQ

C&18 up 1% YoY and down 2% QOQ

● CRE8 up 4% YoY and flat QoQ

• Average deposits of $262B, down 6% YoY, primarily driven

by lower non-operating deposits

Flat QoQ, as client balances are seasonally higher at year-

end

7View entire presentation