Investor Insights: Q1 MCR Corp

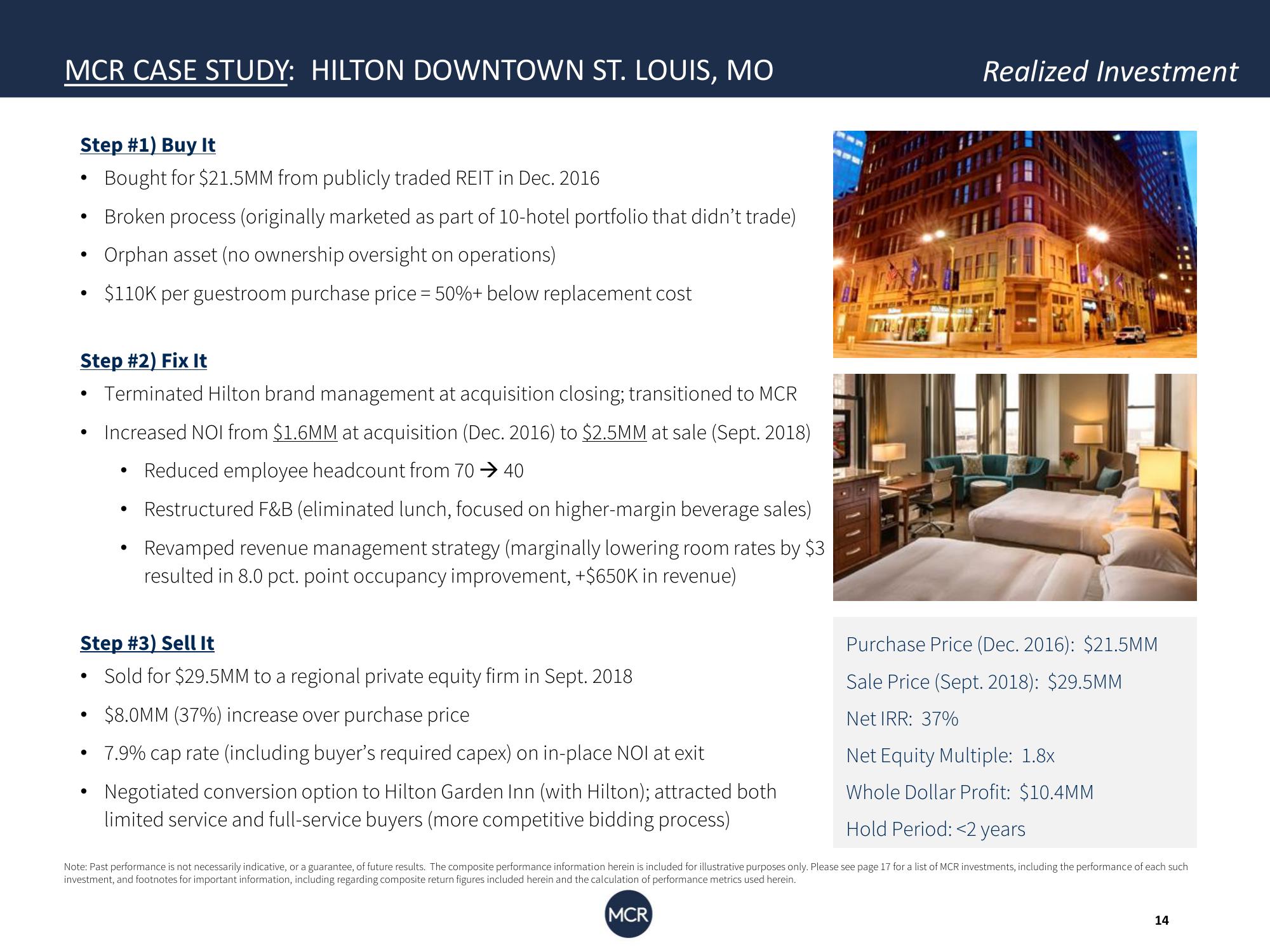

MCR CASE STUDY: HILTON DOWNTOWN ST. LOUIS, MO

Step #1) Buy It

Bought for $21.5MM from publicly traded REIT in Dec. 2016

Broken process (originally marketed as part of 10-hotel portfolio that didn't trade)

Orphan asset (no ownership oversight on operations)

$110K per guestroom purchase price = 50%+ below replacement cost

Step #2) Fix It

Terminated Hilton brand management at acquisition closing; transitioned to MCR

Increased NOI from $1.6MM at acquisition (Dec. 2016) to $2.5MM at sale (Sept. 2018)

Reduced employee headcount from 70 →40

Restructured F&B (eliminated lunch, focused on higher-margin beverage sales)

Revamped revenue management strategy (marginally lowering room rates by $3

resulted in 8.0 pct. point occupancy improvement, +$650K in revenue)

●

●

●

●

Step #3) Sell It

Sold for $29.5MM to a regional private equity firm in Sept. 2018

$8.0MM (37%) increase over purchase price

7.9% cap rate (including buyer's required capex) on in-place NOI at exit

Negotiated conversion option to Hilton Garden Inn (with Hilton); attracted both

limited service and full-service buyers (more competitive bidding process)

Realized Investment

Purchase Price (Dec. 2016): $21.5MM

Sale Price (Sept. 2018): $29.5MM

Net IRR: 37%

Net Equity Multiple: 1.8x

Whole Dollar Profit: $10.4MM

Hold Period: <2 years

Note: Past performance is not necessarily indicative, or a guarantee, of future results. The composite performance information herein is included for illustrative purposes only. Please see page 17 for a list of MCR investments, including the performance of each such

investment, and footnotes for important information, including regarding composite return figures included herein and the calculation of performance metrics used herein.

MCR

14View entire presentation