J.P.Morgan 2Q23 Investor Results

JPMORGAN CHASE & CO.

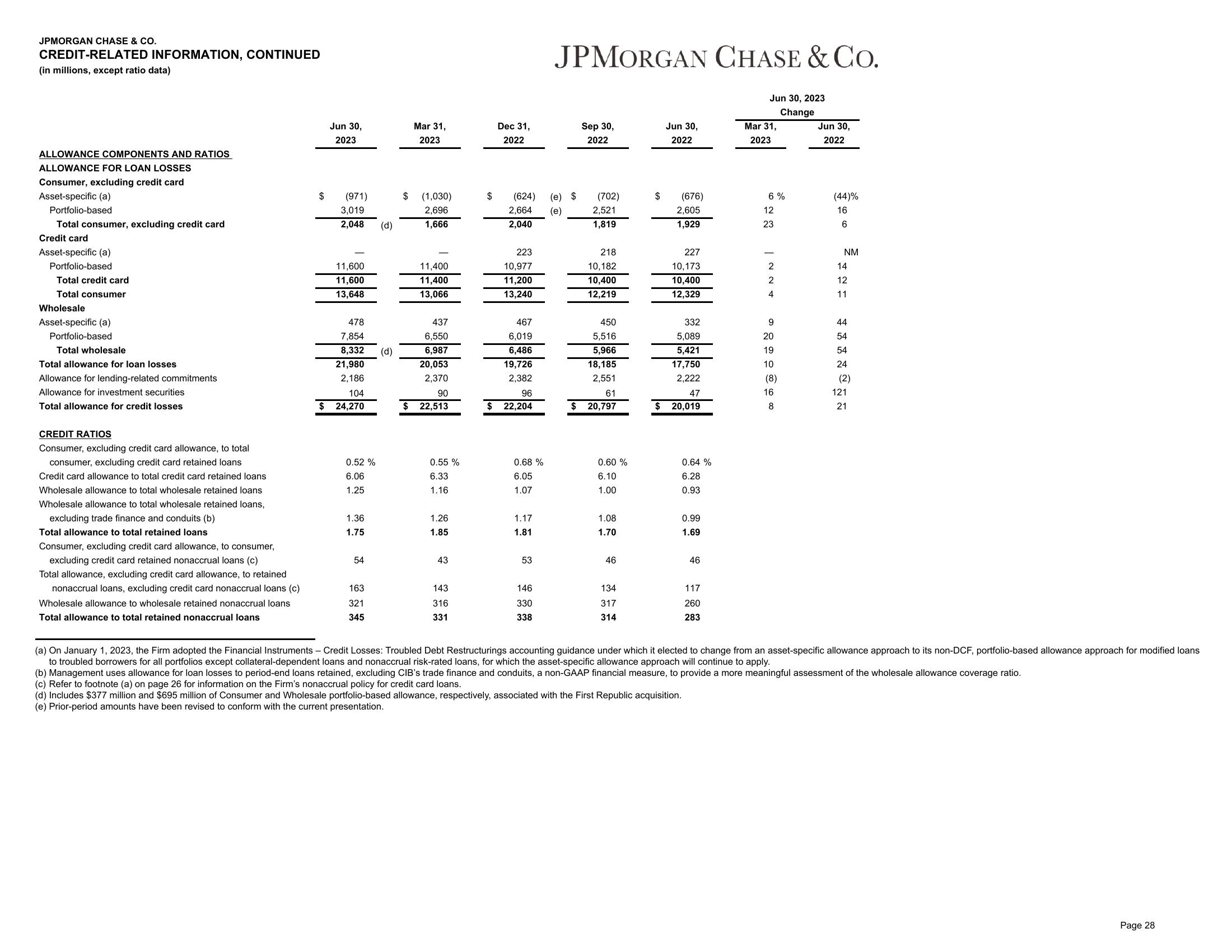

CREDIT-RELATED INFORMATION, CONTINUED

(in millions, except ratio data)

ALLOWANCE COMPONENTS AND RATIOS

ALLOWANCE FOR LOAN LOSSES

Consumer, excluding credit card

Asset-specific (a)

Portfolio-based

Total consumer, excluding credit card

Credit card

Asset-specific (a)

Portfolio-based

Total credit card

Total consumer

Wholesale

Asset-specific (a)

Portfolio-based

Total wholesale

Total allowance for loan losses

Allowance for lending-related commitments

Allowance for investment securities

Total allowance for credit losses

CREDIT RATIOS

Consumer, excluding credit card allowance, to total

consumer, excluding credit card retained loans

Credit card allowance to total credit card retained loans

Wholesale allowance to total wholesale retained loans

Wholesale allowance to total wholesale retained loans,

excluding trade finance and conduits (b)

Total allowance to total retained loans

Consumer, excluding credit card allowance, to consumer,

excluding credit card retained nonaccrual loans (c)

Total allowance, excluding credit card allowance, to retained

nonaccrual loans, excluding credit card nonaccrual loans (c)

Wholesale allowance to wholesale retained nonaccrual loans

Total allowance to total retained nonaccrual loans

$

Jun 30,

2023

(971)

3,019

2,048

11,600

11,600

13,648

478

7,854

8,332 (d)

21,980

2,186

104

24,270

0.52 %

6.06

1.25

1.36

1.75

54

(d)

163

321

345

$

Mar 31,

2023

(1,030)

2,696

1,666

11,400

11,400

13,066

437

6,550

6,987

20,053

2,370

90

$ 22,513

0.55 %

6.33

1.16

1.26

1.85

43

143

316

331

$

Dec 31,

2022

(624)

2,664

2,040

223

10,977

11,200

13,240

467

6,019

6,486

19,726

2,382

96

$ 22,204

0.68 %

6.05

1.07

1.17

1.81

53

146

330

338

JPMORGAN CHASE & CO.

(e) $

(e)

Sep 30,

2022

(702)

2,521

1,819

218

10,182

10,400

12,219

450

5,516

5,966

18,185

2,551

61

$ 20,797

0.60 %

6.10

1.00

1.08

1.70

4465

134

317

314

$

$

Jun 30,

2022

(676)

2,605

1,929

227

10,173

10,400

12,329

332

5,089

5,421

17,750

2,222

47

20,019

0.64 %

6.28

0.93

0.99

1.69

46

117

260

283

Jun 30, 2023

Change

Mar 31,

2023

6%

12

23

| N24

9

20

19

10

(8)

16

8

Jun 30,

2022

(44)%

²+2= $***^¯Ñ

NM

(a) On January 1, 2023, the Firm adopted the Financial Instruments - Credit Losses: Troubled Debt Restructurings accounting guidance under which it elected to change from an asset-specific allowance approach to its non-DCF, portfolio-based allowance approach for modified loans

to troubled borrowers for all portfolios except collateral-dependent loans and nonaccrual risk-rated loans, for which the asset-specific allowance approach will continue to apply.

(b) Management uses allowance for loan losses to period-end loans retained, excluding CIB's trade finance and conduits, a non-GAAP financial measure, to provide a more meaningful assessment of the wholesale allowance coverage ratio.

(c) Refer to footnote (a) on page 26 for information on the Firm's nonaccrual policy for credit card loans.

(d) Includes $377 million and $695 million of Consumer and Wholesale portfolio-based allowance, respectively, associated with the First Republic acquisition.

(e) Prior-period amounts have been revised to conform with the current presentation.

Page 28View entire presentation