Pathward Financial Results Presentation Deck

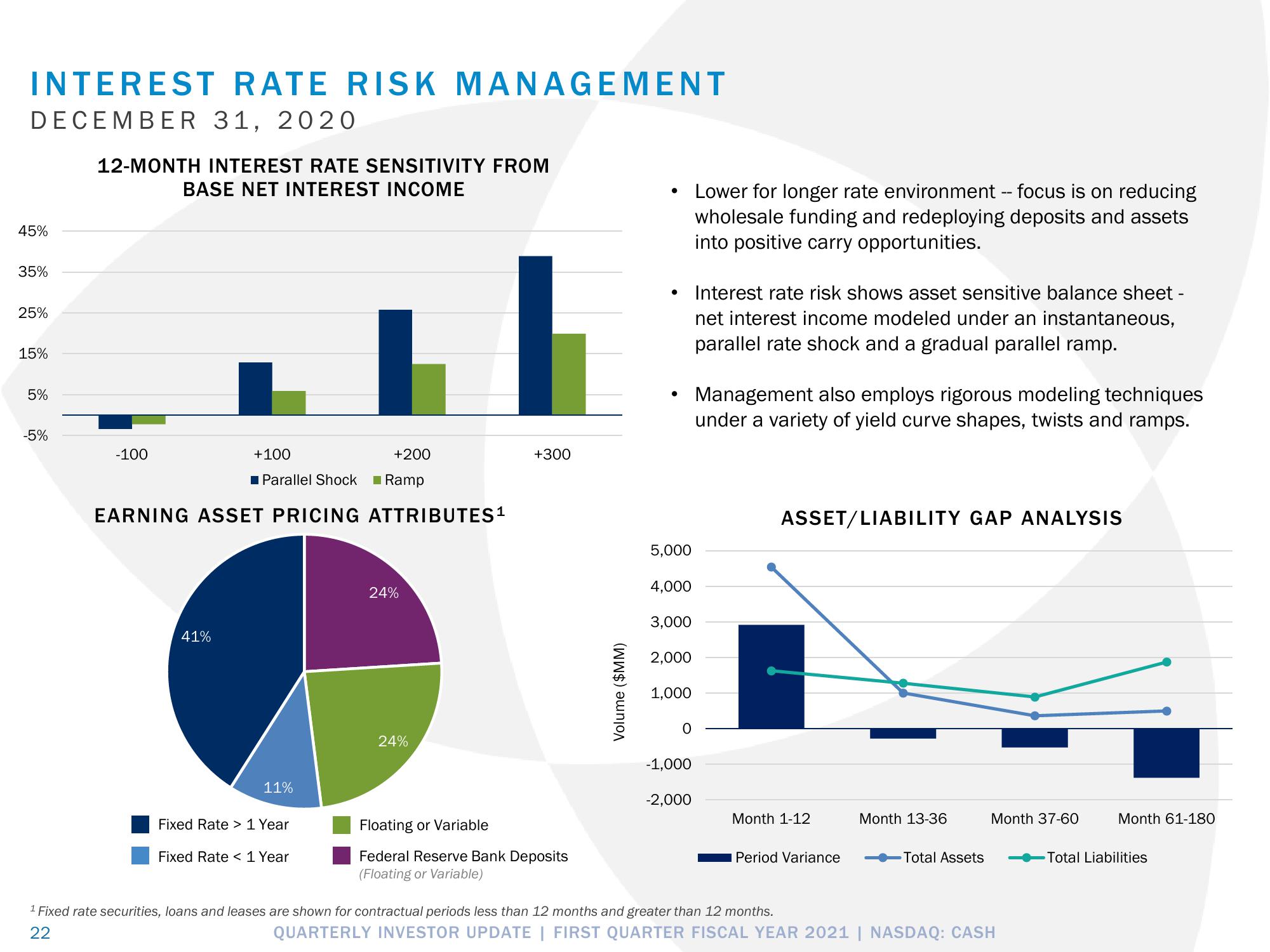

INTEREST RATE RISK MANAGEMENT

DECEMBER 31, 2020

45%

35%

25%

15%

5%

-5%

12-MONTH INTEREST RATE SENSITIVITY FROM

BASE NET INTEREST INCOME

-100

+100

+200

Parallel Shock ■ Ramp

EARNING ASSET PRICING ATTRIBUTES ¹

41%

11%

Fixed Rate > 1 Year

Fixed Rate < 1 Year

24%

24%

+300

Floating or Variable

Federal Reserve Bank Deposits

(Floating or Variable)

Volume ($MM)

• Interest rate risk shows asset sensitive balance sheet -

net interest income modeled under an instantaneous,

parallel rate shock and a gradual parallel ramp.

5,000

4,000

3,000

2,000

1,000

O

-1,000

Lower for longer rate environment -- focus is on reducing

wholesale funding and redeploying deposits and assets

into positive carry opportunities.

-2,000

Management also employs rigorous modeling techniques

under a variety of yield curve shapes, twists and ramps.

ASSET/LIABILITY GAP ANALYSIS

Month 1-12

Period Variance

Month 13-36

Total Assets

Month 37-60

¹ Fixed rate securities, loans and leases are shown for contractual periods less than 12 months and greater than 12 months.

22

QUARTERLY INVESTOR UPDATE | FIRST QUARTER FISCAL YEAR 2021 | NASDAQ: CASH

Month 61-180

Total LiabilitiesView entire presentation