Lyft Investor Presentation Deck

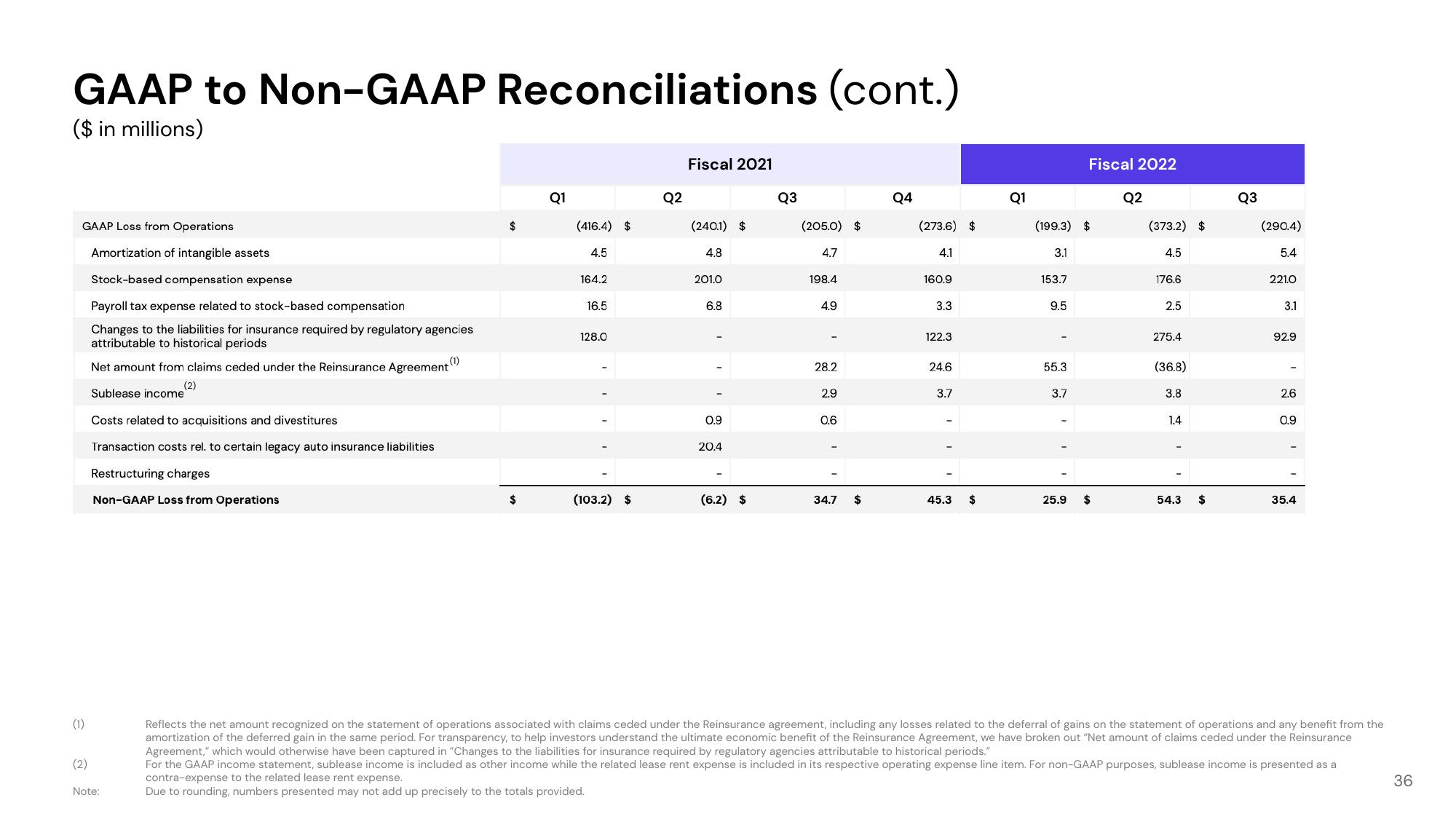

GAAP to Non-GAAP Reconciliations (cont.)

($ in millions)

GAAP Loss from Operations

Amortization of intangible assets

Stock-based compensation expense

(1)

(2)

Payroll tax expense related to stock-based compensation

Changes to the liabilities for insurance required by regulatory agencies

attributable to historical periods

Net amount from claims ceded under the Reinsurance Agreement (1)

(2)

Sublease income

Costs related to acquisitions and divestitures

Transaction costs rel. to certain legacy auto insurance liabilities

Restructuring charges

Non-GAAP Loss from Operations

Note:

$

$

Q1

(416.4) $

4.5

164.2

16.5

128.0

(103.2) $

Q2

Fiscal 2021

(2401) $

4.8

201.0

6.8

0.9

20.4

(6.2) $

Q3

(205.0) $

4.7

198.4

4.9

28.2

2.9

0.6

34.7 $

Q4

(273.6) $

4.1

160.9

3.3

122.

24.6

3.7

45.3 $

Q1

(199.3) $

3.1

153.7

9.5

55.3

Fiscal 2022

3.7

25.9 $

Q2

(373.2) $

4.5

176.6

2.5

275.4

(36.8)

3.8

1.4

54.3 $

Q3

(290.4)

5.4

221.0

3.1

92.9

2.6

0.9

35.4

Reflects the net amount recognized on the statement of operations associated with claims ceded under the Reinsurance agreement, including any losses related to the deferral of gains on the statement of operations and any benefit from the

amortization of the deferred gain in the same period. For transparency, to help investors understand the ultimate economic benefit of the Reinsurance Agreement, we have broken out "Net amount of claims ceded under the Reinsurance

Agreement," which would otherwise have been captured in "Changes to the liabilities for insurance required by regulatory agencies attributable to historical periods."

For the GAAP income statement, sublease income is included as other income while the related lease rent expense is included in its respective operating expense line item. For non-GAAP purposes, sublease income is presented as a

contra-expense to the related lease rent expense.

Due to rounding, numbers presented may not add up precisely to the totals provided.

36View entire presentation