J.P.Morgan Results Presentation Deck

JPMORGAN CHASE & CO.

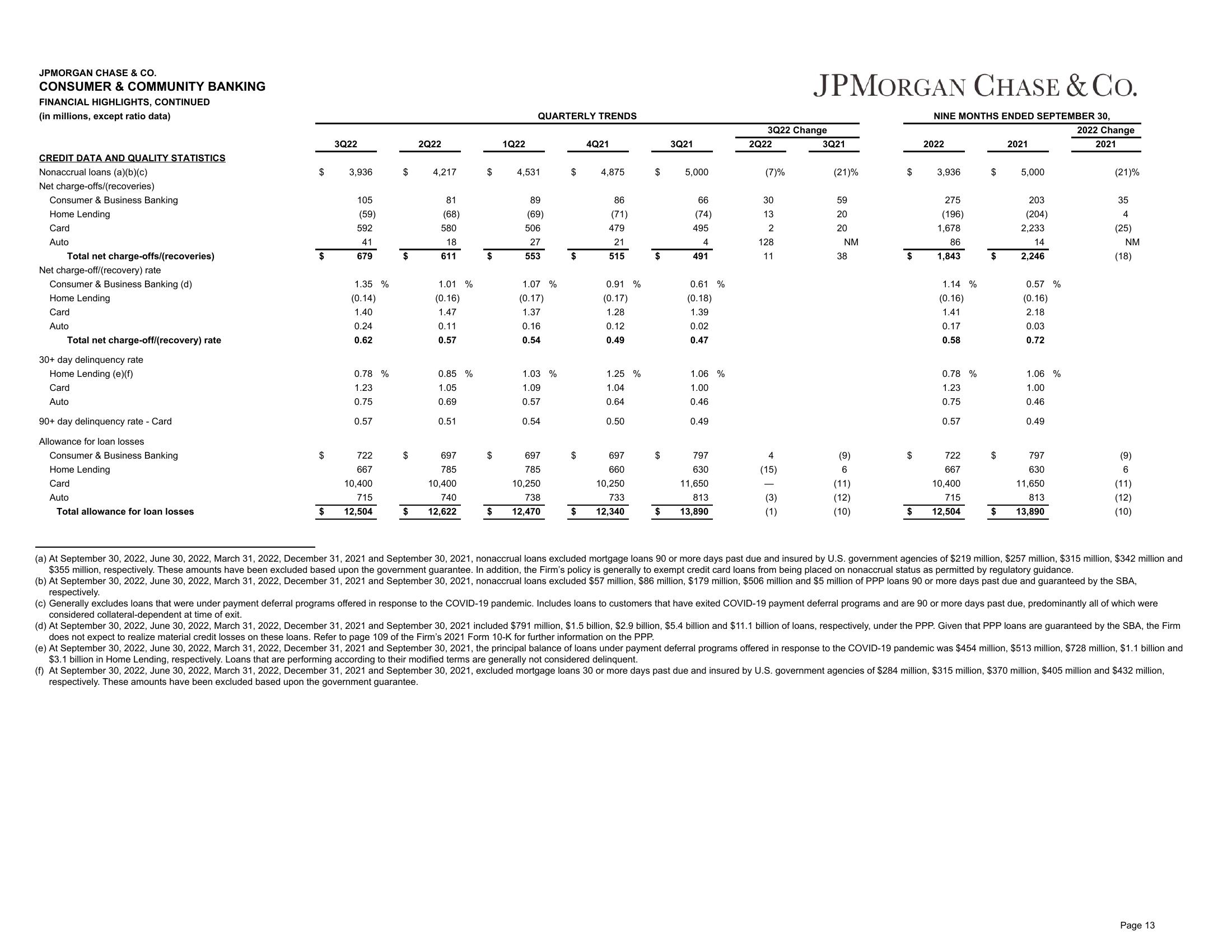

CONSUMER & COMMUNITY BANKING

FINANCIAL HIGHLIGHTS, CONTINUED

(in millions, except ratio data)

CREDIT DATA AND QUALITY STATISTICS

Nonaccrual loans (a)(b)(c)

Net charge-offs/(recoveries)

Consumer & Business Banking

Home Lending

Card

Auto

Total net charge-offs/(recoveries)

Net charge-off/(recovery) rate

Consumer & Business Banking (d)

Home Lending

Card

Auto

Total net charge-off/(recovery) rate

30+ day delinquency rate

Home Lending (e)(f)

Card

Auto

90+ day delinquency rate - Card

Allowance for loan losses

Consumer & Business Banking

Home Lending

Card

Auto

Total allowance for loan losses

$

$

$

$

3Q22

3,936

105

(59)

592

41

679

1.35 %

(0.14)

1.40

0.24

0.62

0.78 %

1.23

0.75

0.57

722

667

10,400

715

12,504

$

$

$

2Q22

4,217

81

(68)

580

18

611

1.01 %

(0.16)

1.47

0.11

0.57

0.85 %

1.05

0.69

0.51

697

785

10,400

740

12,622

$

$

$

1Q22

QUARTERLY TRENDS

4,531

89

(69)

506

27

553

1.07 %

(0.17)

1.37

0.16

0.54

1.03 %

1.09

0.57

0.54

697

785

10,250

738

12,470

$

$

$

4Q21

4,875

86

(71)

479

21

515

0.91 %

(0.17)

1.28

0.12

0.49

1.25 %

1.04

0.64

0.50

697

660

10,250

733

12,340

$

$

$

$

3Q21

5,000

66

(74)

495

4

491

0.61 %

(0.18)

1.39

0.02

0.47

1.06 %

1.00

0.46

0.49

797

630

11,650

813

13,890

3Q22 Change

2Q22

(7)%

30

13

2

128

11

4

(15)

|

JPMORGAN CHASE & CO.

(3)

(1)

3Q21

(21)%

59

20

20

NM

38

(9)

6

(11)

(12)

(10)

$

$

$

$

NINE MONTHS ENDED SEPTEMBER 30,

2022

3,936

275

(196)

1,678

86

1,843

1.14 %

(0.16)

1.41

0.17

0.58

0.78 %

1.23

0.75

0.57

722

667

10,400

715

12,504

$

$

$

$

2021

5,000

203

(204)

2,233

14

2,246

0.57 %

(0.16)

2.18

0.03

0.72

1.06 %

1.00

0.46

0.49

797

630

11,650

813

13,890

2022 Change

2021

(21)%

35

4

(25)

NM

(18)

(9)

6

(11)

(12)

(10)

(a) At September 30, 2022, June 30, 2022, March 31, 2022, December 31, 2021 and September 30, 2021, nonaccrual loans excluded mortgage loans 90 or more days past due and insured by U.S. government agencies of $219 million, $257 million, $315 million, $342 million and

$355 million, respectively. These amounts have been excluded based upon the government guarantee. In addition, the Firm's policy is generally to exempt credit card loans from being placed on nonaccrual status as permitted by regulatory guidance.

(b) At September 30, 2022, June 30, 2022, March 31, 2022, December 31, 2021 and September 30, 2021, nonaccrual loans excluded $57 million, $86 million, $179 million, $506 million and $5 million of PPP loans 90 or more days past due and guaranteed by the SBA,

respectively.

(c) Generally excludes loans that were under payment deferral programs offered in response to the COVID-19 pandemic. Includes loans to customers that have exited COVID-19 payment deferral programs and are 90 or more days past due, predominantly all of which were

considered collateral-dependent at time of exit.

(d) At September 30, 2022, June 30, 2022, March 31, 2022, December 31, 2021 and September 30, 2021 included $791 million, $1.5 billion, $2.9 billion, $5.4 billion and $11.1 billion of loans, respectively, under the PPP. Given that PPP loans are guaranteed by the SBA, the Firm

does not expect to realize material credit losses on these loans. Refer to page 109 of the Firm's 2021 Form 10-K for further information on the PPP.

(e) At September 30, 2022, June 30, 2022, March 31, 2022, December 31, 2021 and September 30, 2021, the principal balance of loans under payment deferral programs offered in response to the COVID-19 pandemic was $454 million, $513 million, $728 million, $1.1 billion and

$3.1 billion in Home Lending, respectively. Loans that are performing according to their modified terms are generally not considered delinquent.

(f) At September 30, 2022, June 30, 2022, March 31, 2022, December 31, 2021 and September 30, 2021, excluded mortgage loans 30 or more days past due and insured by U.S. government agencies of $284 million, $315 million, $370 million, $405 million and $432 million,

respectively. These amounts have been excluded based upon the government guarantee.

Page 13View entire presentation