Hexagon Purus SPAC Presentation Deck

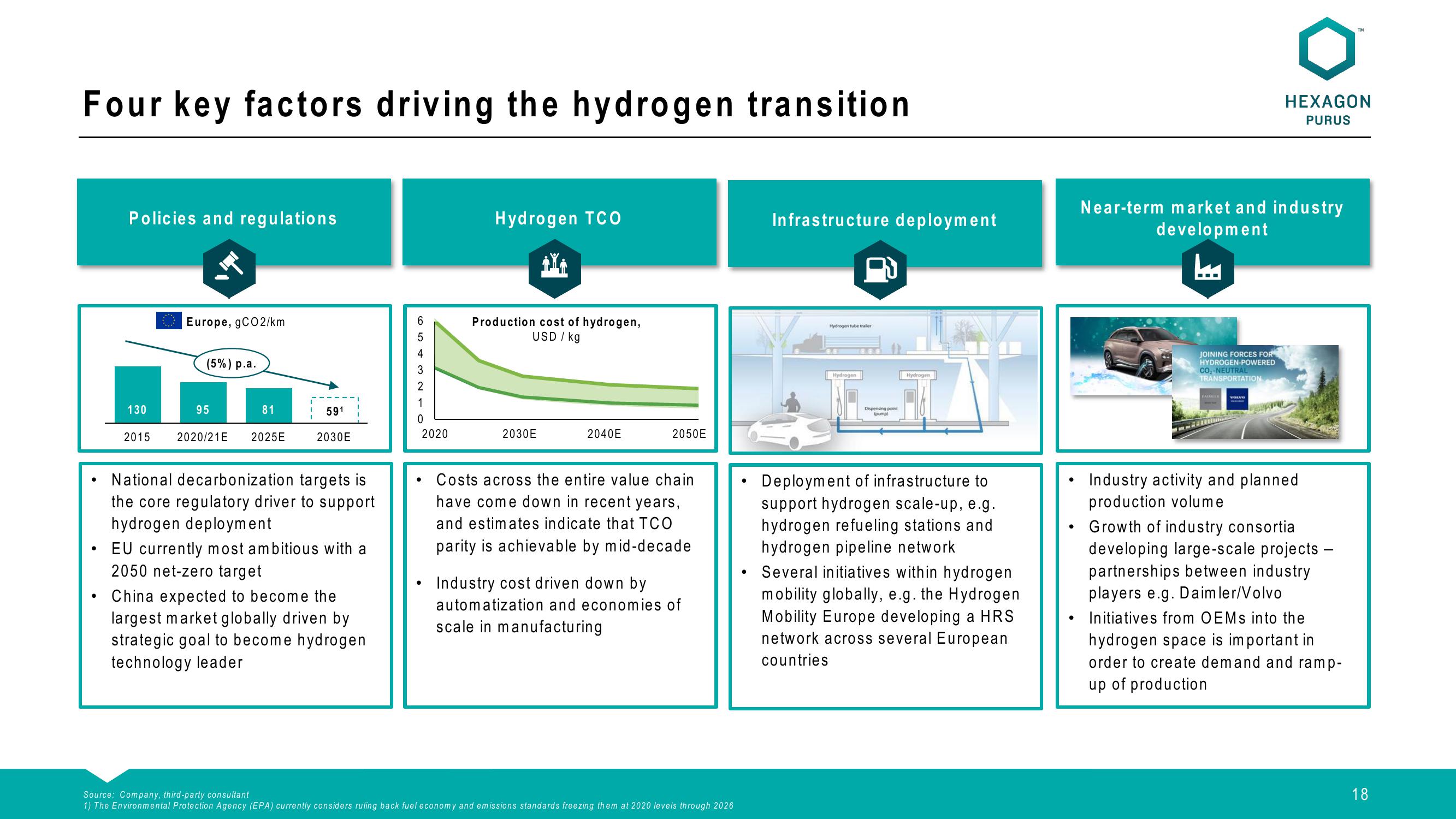

Four key factors driving the hydrogen transition

Policies and regulations

130

2015

Europe, gCO2/km

(5%) p.a.

95

81

2020/21E 2025E

591

2030E

National decarbonization targets is

the core regulatory driver to support

hydrogen deployment

• EU currently most ambitious with a

2050 net-zero target

• China expected to become the

largest market globally driven by

strategic goal to become hydrogen

technology leader

C543

6

2

1

0

2020

●

Hydrogen TCO

Production cost of hydrogen,

USD / kg

2030E

2040E

2050E

Costs across the entire value chain

have come down in recent years,

and estimates indicate that TCO

parity is achievable by mid-decade

Industry cost driven down by

automatization and economies of

scale in manufacturing

Source: Company, third-party consultant

1) The Environmental Protection Agency (EPA) currently considers ruling back fuel economy and emissions standards freezing them at 2020 levels through 2026

●

Infrastructure deployment

Hydrogen tube trailer

Hydrogen

Dispensing point

(pump)

7

Hydrogen

Deployment of infrastructure to

support hydrogen scale-up, e.g.

hydrogen refueling stations and

hydrogen pipeline network

Several initiatives within hydrogen

mobility globally, e.g. the Hydrogen

Mobility Europe developing a HRS

network across several European

countries

Near-term market and industry

development

ما

JOINING FORCES FOR

HYDROGEN-POWERED

CO₂-NEUTRAL

TRANSPORTATION

HEXAGON

PURUS

Industry activity and planned

production volume

TM

Growth of industry consortia

developing large-scale projects -

partnerships between industry

players e.g. Daimler/Volvo

Initiatives from OEMs into the

hydrogen space is important in

order to create demand and ramp-

up of production

18View entire presentation