Coppersmith Presentation to Alere Inc Stockholders

PAGE 32 |

COPPERSMITH

The Truth About Coppersmith's Plan for HM 1

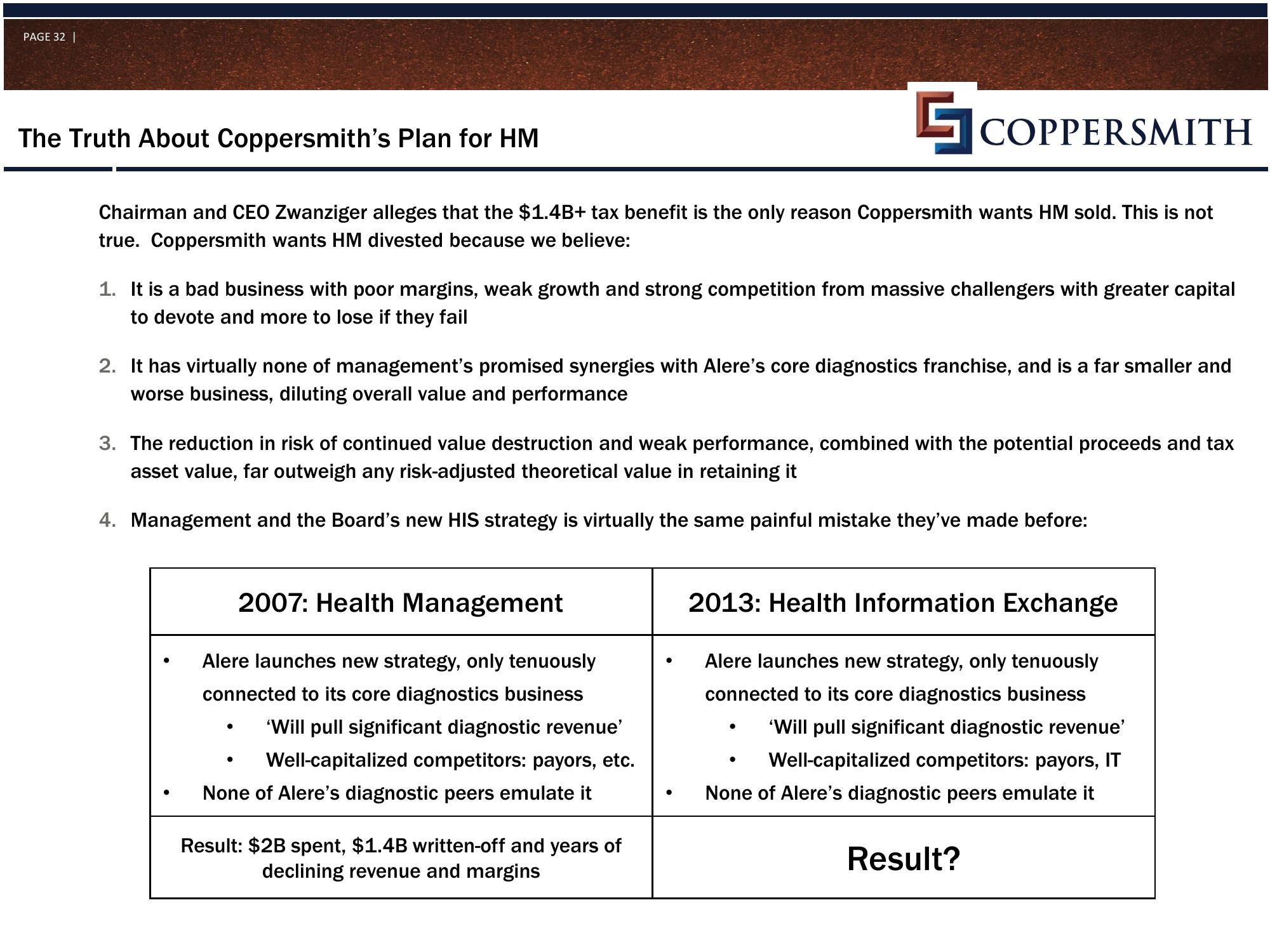

Chairman and CEO Zwanziger alleges that the $1.4B+ tax benefit is the only reason Coppersmith wants HM sold. This is not

true. Coppersmith wants HM divested because we believe:

1. It is a bad business with poor margins, weak growth and strong competition from massive challengers with greater capital

to devote and more to lose if they fail

2. It has virtually none of management's promised synergies with Alere's core diagnostics franchise, and is a far smaller and

worse business, diluting overall value and performance

3. The reduction in risk of continued value destruction and weak performance, combined with the potential proceeds and tax

asset value, far outweigh any risk-adjusted theoretical value in retaining it

4. Management and the Board's new HIS strategy is virtually the same painful mistake they've made before:

2007: Health Management

Alere launches new strategy, only tenuously

connected to its core diagnostics business

'Will pull significant diagnostic revenue'

Well-capitalized competitors: payors, etc.

None of Alere's diagnostic peers emulate it

Result: $2B spent, $1.4B written-off and years of

declining revenue and margins

2013: Health Information Exchange

Alere launches new strategy, only tenuously

connected to its core diagnostics business

'Will pull significant diagnostic revenue'

Well-capitalized competitors: payors, IT

None of Alere's diagnostic peers emulate it

Result?View entire presentation