Melrose Results Presentation Deck

Powder Metallurgy: overview

Melrose

£m

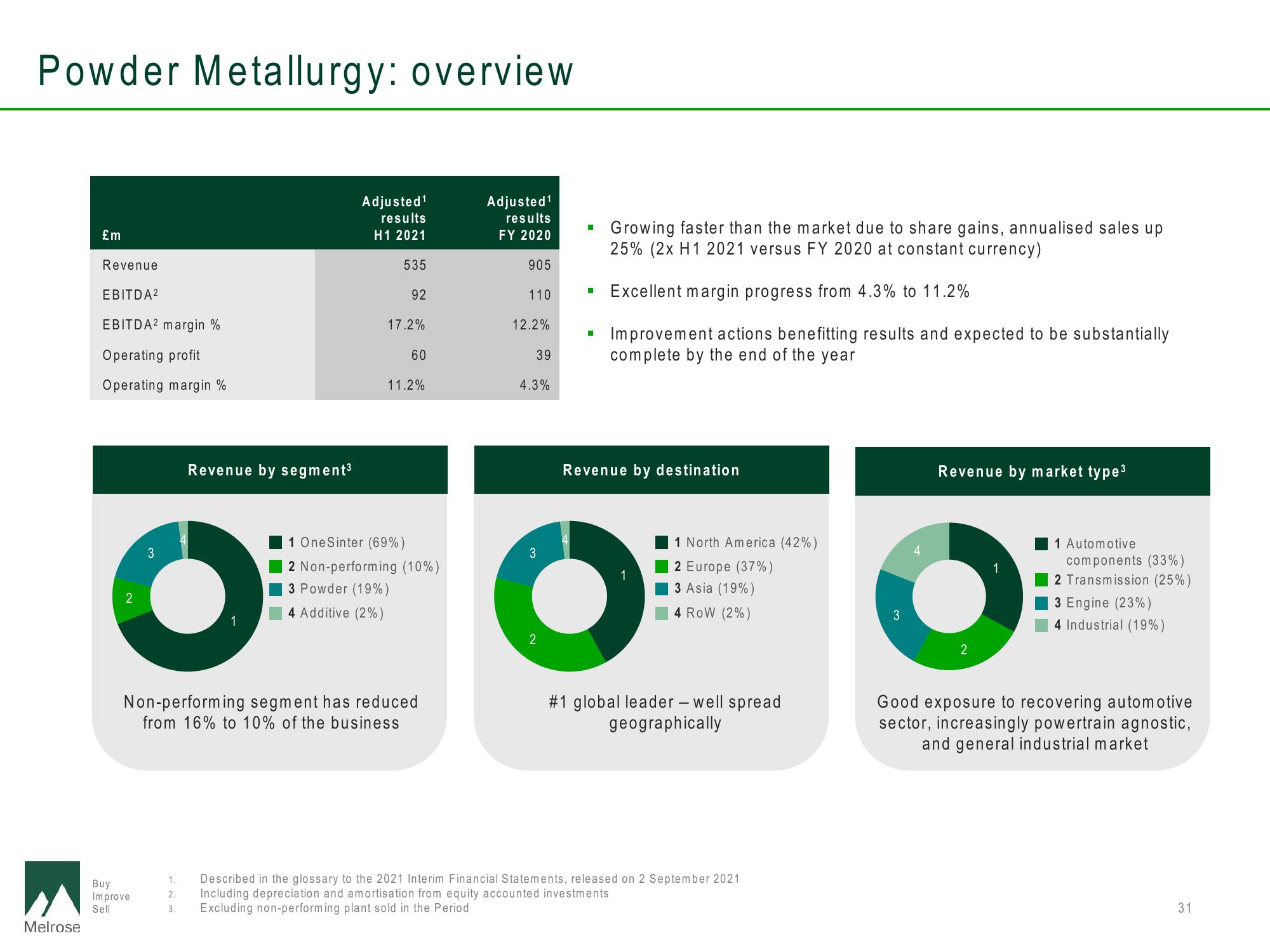

Revenue

EBITDA²

EBITDA2 margin %

Operating profit

Operating margin %

2

3

Buy

Improve

Sell

Revenue by segment³

Adjusted ¹

results

H1 2021

535

92

17.2%

60

11.2%

1 OneSinter (69%)

2 Non-performing (10%)

3 Powder (19%)

4 Additive (2%)

Non-performing segment has reduced

from 16% to 10% of the business

Adjusted¹

results

FY 2020

905

110

12.2%

39

4.3%

3

2

■

■

Growing faster than the market due to share gains, annualised sales up

25% (2x H1 2021 versus FY 2020 at constant currency)

Excellent margin progress from 4.3% to 11.2%

Improvement actions benefitting results and expected to be substantially

complete by the end of the year

Revenue by destination

1

1 North America (42%)

2 Europe (37%)

3 Asia (19%)

4 ROW (2%)

#1 global leader - well spread

geographically

1.

Described in the glossary to the 2021 Interim Financial Statements, released on 2 September 2021

2.

Including depreciation and amortisation from equity accounted investments

3. Excluding non-performing plant sold in the Period

Revenue by market type³

2

1 Automotive

components (33%)

2 Transmission (25%)

3 Engine (23%)

4 Industrial (19%)

Good exposure to recovering automotive

sector, increasingly powertrain agnostic,

and general industrial market

31View entire presentation