Pathward Financial Results Presentation Deck

Interest Rate Risk Management September 30, 2023

24

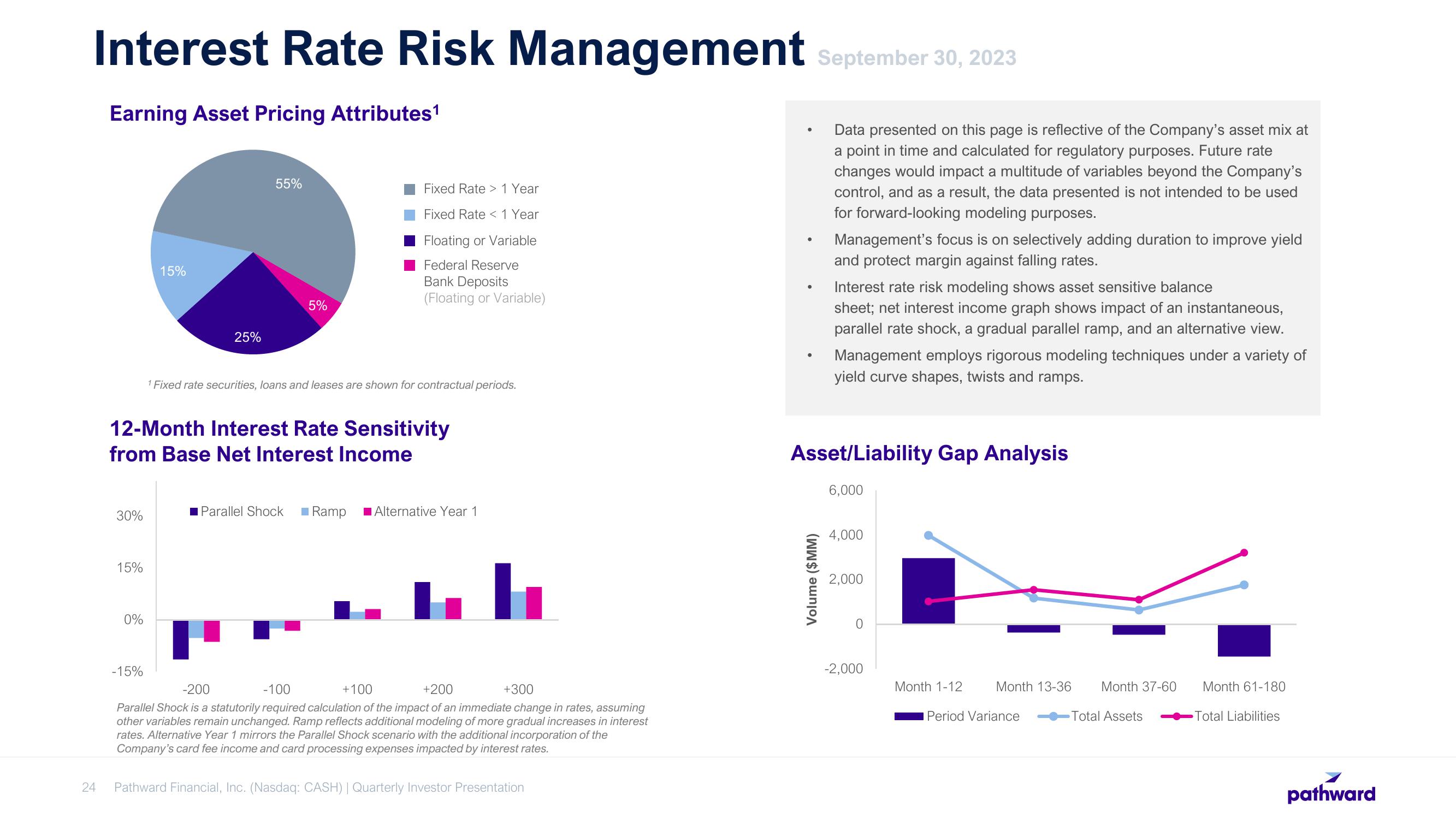

Earning Asset Pricing Attributes¹

30%

15%

0%

15%

-15%

25%

55%

12-Month Interest Rate Sensitivity

from Base Net Interest Income

5%

Fixed Rate > 1 Year

Fixed Rate < 1 Year

Floating or Variable

Federal Reserve

Bank Deposits

(Floating or Variable)

¹ Fixed rate securities, loans and leases are shown for contractual periods.

Parallel Shock ■Ramp ■Alternative Year 1

+100

+200

+300

-200

-100

Parallel Shock is a statutorily required calculation of the impact of an immediate change in rates, assuming

other variables remain unchanged. Ramp reflects additional modeling of more gradual increases in interest

rates. Alternative Year 1 mirrors the Parallel Shock scenario with the additional incorporation of the

Company's card fee income and card processing expenses impacted by interest rates.

Pathward Financial, Inc. (Nasdaq: CASH) | Quarterly Investor Presentation

Data presented on this page is reflective of the Company's asset mix at

a point in time and calculated for regulatory purposes. Future rate

changes would impact a multitude of variables beyond the Company's

control, and as a result, the data presented is not intended to be used

for forward-looking modeling purposes.

Volume ($MM)

Management's focus is on selectively adding duration to improve yield

and protect margin against falling rates.

Interest rate risk modeling shows asset sensitive balance

sheet; net interest income graph shows impact of an instantaneous,

parallel rate shock, a gradual parallel ramp, and an alternative view.

Management employs rigorous modeling techniques under a variety of

yield curve shapes, twists and ramps.

Asset/Liability Gap Analysis

6,000

4,000

2,000

-2,000

Month 1-12

Month 13-36

Period Variance

Month 37-60

-Total Assets

Month 61-180

Total Liabilities

pathwardView entire presentation