J.P.Morgan 4Q23 Earnings Results

JPMORGAN CHASE & CO.

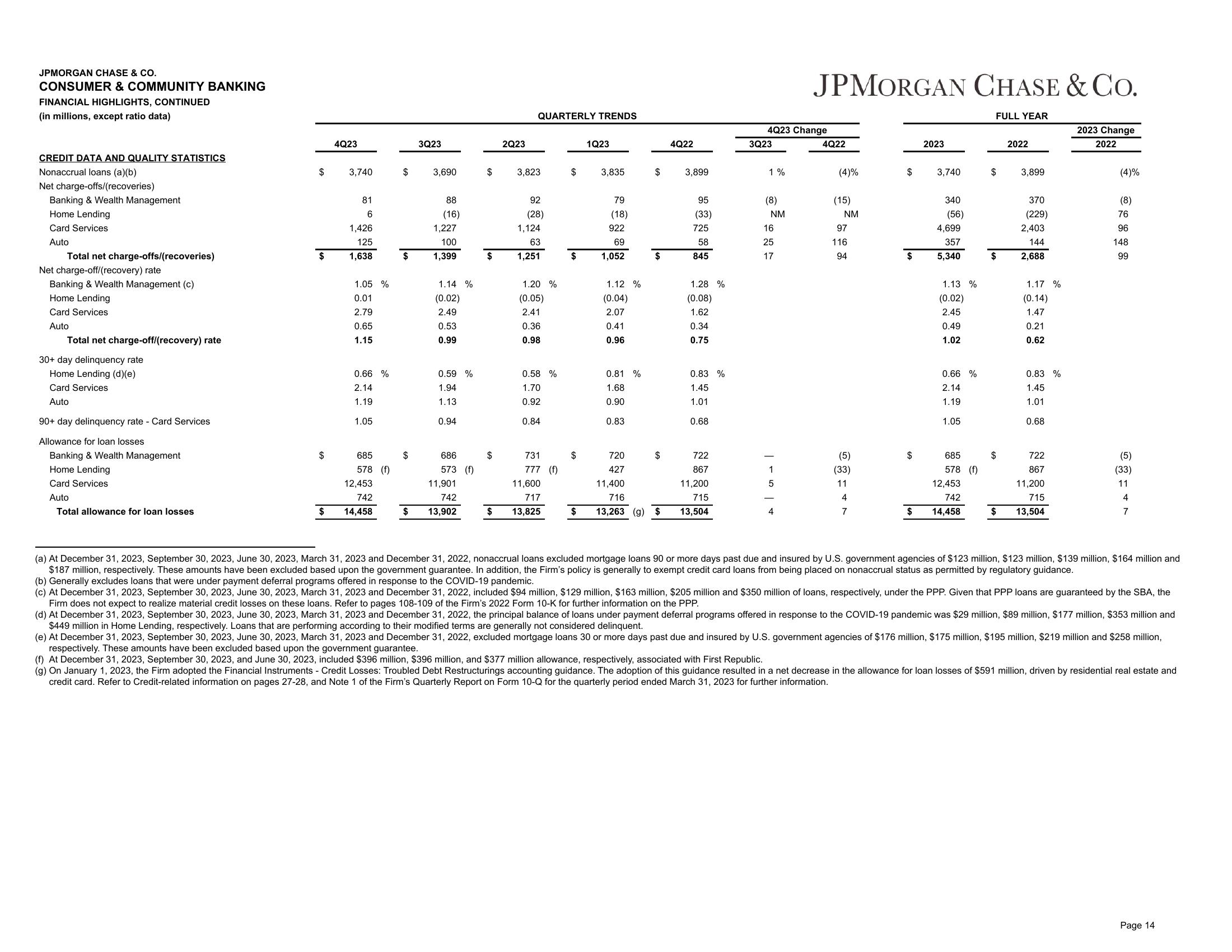

CONSUMER & COMMUNITY BANKING

FINANCIAL HIGHLIGHTS, CONTINUED

(in millions, except ratio data)

CREDIT DATA AND QUALITY STATISTICS

Nonaccrual loans (a)(b)

Net charge-offs/(recoveries)

Banking & Wealth Management

Home Lending

Card Services

Auto

Total net charge-offs/(recoveries)

Net charge-off/(recovery) rate

Banking & Wealth Management (c)

Home Lending

Card Services

Auto

Total net charge-off/(recovery) rate

30+ day delinquency rate

Home Lending (d)(e)

Card Services

Auto

90+ day delinquency rate - Card Services

Allowance for loan losses

Banking & Wealth Management

Home Lending

Card Services

Auto

Total allowance for loan losses

$

$

$

$

4Q23

3,740

81

6

1,426

125

1,638

1.05 %

0.01

2.79

0.65

1.15

0.66 %

2.14

1.19

1.05

685

578 (f)

12,453

742

14,458

$

$

$

3Q23

3,690

88

(16)

1,227

100

1,399

1.14 %

(0.02)

2.49

0.53

0.99

0.59%

1.94

1.13

0.94

686

573 (f)

11,901

742

13,902

$

$

$

2Q23

QUARTERLY TRENDS

3,823

92

(28)

1,124

63

1,251

1.20 %

(0.05)

2.41

0.36

0.98

0.58 %

1.70

0.92

0.84

731

777 (f)

11,600

717

13,825

$

$

$

1Q23

3,835

79

(18)

922

69

1,052

1.12 %

(0.04)

2.07

0.41

0.96

0.81 %

1.68

0.90

0.83

720

427

$

$

$

11,400

716

13,263 (g) $

4Q22

3,899

95

(33)

725

58

845

1.28 %

(0.08)

1.62

0.34

0.75

0.83 %

1.45

1.01

0.68

722

867

11,200

715

13,504

4Q23 Change

3Q23

1%

(8)

NM

16

25

17

JPMORGAN CHASE & CO.

| ܝ ܗ | ܟ

4Q22

(4)%

(15)

NM

97

116

94

(5)

(33)

11

4

7

$

$

$

$

2023

3,740

340

(56)

4,699

357

5,340

1.13 %

(0.02)

2.45

0.49

1.02

0.66 %

2.14

1.19

1.05

685

578 (f)

12,453

742

14,458

FULL YEAR

$

$

$

2022

3,899

370

(229)

2,403

144

2,688

1.17 %

(0.14)

1.47

0.21

0.62

0.83 %

1.45

1.01

0.68

722

867

11,200

715

$ 13,504

2023 Change

2022

(4)%

(8)

76

96

148

99

(5)

(33)

11

4

7

(a) At December 31, 2023, September 30, 2023, June 30, 2023, March 31, 2023 and December 31, 2022, nonaccrual loans excluded mortgage loans 90 or more days past due and insured by U.S. government agencies of $123 million, $123 million, $139 million, $164 million and

$187 million, respectively. These amounts have been excluded based upon the government guarantee. In addition, the Firm's policy is generally to exempt credit card loans from being placed on nonaccrual status as permitted by regulatory guidance.

(b) Generally excludes loans that were under payment deferral programs offered in response to the COVID-19 pandemic.

(c) At December 31, 2023, September 30, 2023, June 30, 2023, March 31, 2023 and December 31, 2022, included $94 million, $129 million, $163 million, $205 million and $350 million of loans, respectively, under the PPP. Given that PPP loans are guaranteed by the SBA, the

Firm does not expect to realize material credit losses on these loans. Refer to pages 108-109 of the Firm's 2022 Form 10-K for further information on the PPP.

(d) At December 31, 2023, September 30, 2023, June 30, 2023, March 31, 2023 and December 31, 2022, the principal balance of loans under payment deferral programs offered in response to the COVID-19 pandemic was $29 million, $89 million, $177 million, $353 million and

$449 million in Home Lending, respectively. Loans that are performing according to their modified terms are generally not considered delinquent.

(e) At December 31, 2023, September 30, 2023, June 30, 2023, March 31, 2023 and December 31, 2022, excluded mortgage loans 30 or more days past due and insured by U.S. government agencies of $176 million, $175 million, $195 million, $219 million and $258 million,

respectively. These amounts have been excluded based upon the government guarantee.

(f) At December 31, 2023, September 30, 2023, and June 30, 2023, included $396 million, $396 million, and $377 million allowance, respectively, associated with First Republic.

(g) On January 1, 2023, the Firm adopted the Financial Instruments - Credit Losses: Troubled Debt Restructurings accounting guidance. The adoption of this guidance resulted in a net decrease in the allowance for loan losses of $591 million, driven by residential real estate and

credit card. Refer to Credit-related information on pages 27-28, and Note 1 of the Firm's Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2023 for further information.

Page 14View entire presentation