J.P.Morgan Results Presentation Deck

Commercial Banking1

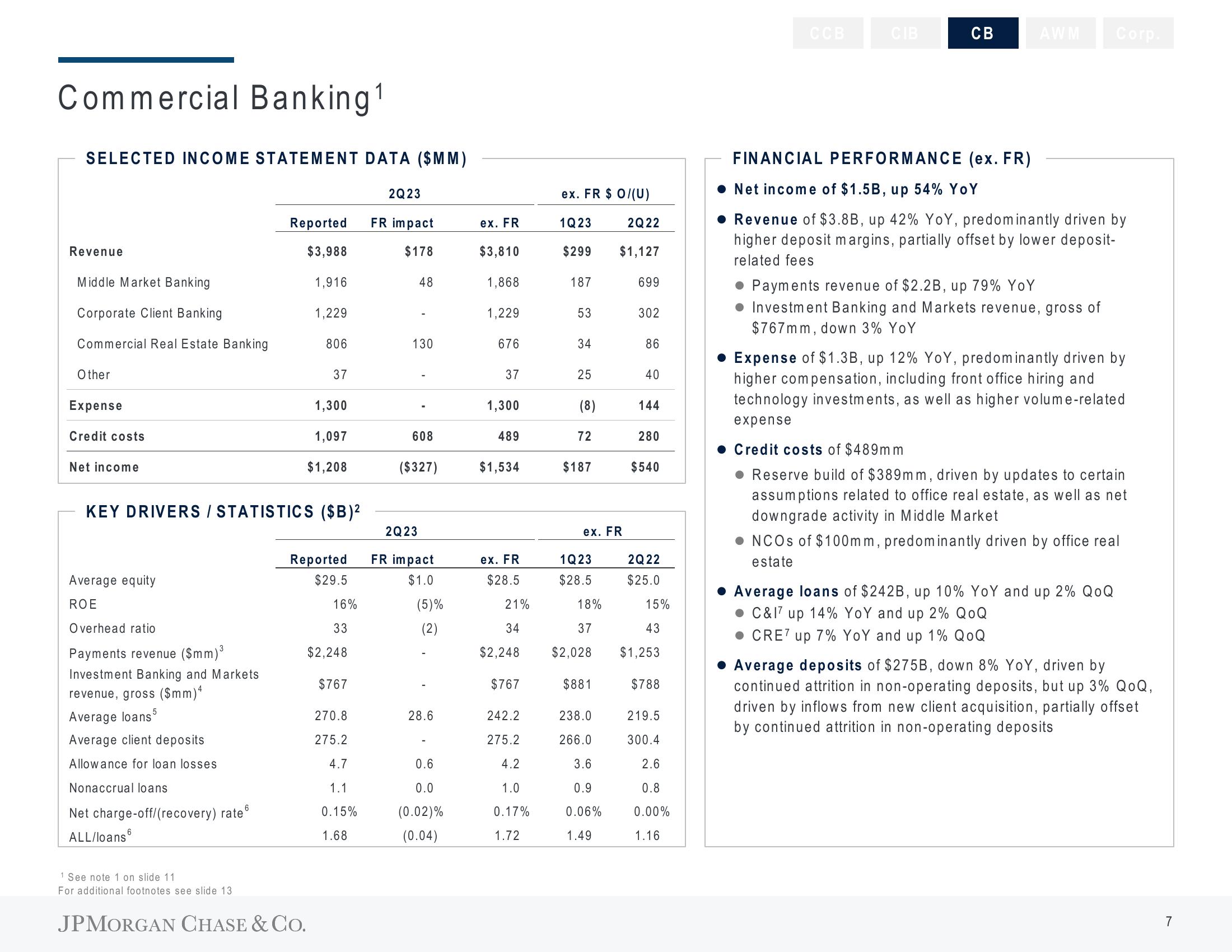

SELECTED INCOME STATEMENT DATA ($MM)

Revenue

Middle Market Banking

Corporate Client Banking

Commercial Real Estate Banking

Other

Expense

Credit costs

Net income

Average equity

ROE

Overhead ratio

Payments revenue ($mm) ³

Investment Banking and Markets

revenue, gross ($mm)4

5

Average loans

Average client deposits

Allowance for loan losses

Nonaccrual loans

Net charge-off/(recovery) rate

ALL/loans

Reported

$3,988

1,916

KEY DRIVERS / STATISTICS ($B)²

1 See note 1 on slide 11

For additional footnotes see slide 13.

1,229

806

JPMORGAN CHASE & CO.

37

1,300

1,097

$1,208

Reported

$29.5

16%

33

$2,248

$767

270.8

275.2

4.7

1.1

0.15%

1.68

2Q23

FR impact

$178

48

130

608

($327)

2Q23

FR impact

$1.0

(5)%

(2)

28.6

0.6

0.0

(0.02)%

(0.04)

ex. FR

$3,810

1,868

1,229

676

37

1,300

489

$1,534

ex. FR

$28.5

21%

34

$2,248

$767

242.2

275.2

4.2

1.0

0.17%

1.72

ex. FR $ 0/(U)

1Q23

$299

187

53

34

25

(8)

72

$187

ex. FR

1Q 23

$28.5

18%

37

$2,028

$881

2Q22

$1,127

238.0

266.0

3.6

0.9

0.06%

1.49

699

302

86

40

144

280

$540

2Q22

$25.0

15%

43

$1,253

$788

219.5

300.4

2.6

0.8

0.00%

1.16

CCB

CIB

CB

AWM Corp.

FINANCIAL PERFORMANCE (ex. FR)

• Net income of $1.5B, up 54% YoY

• Revenue of $3.8B, up 42% YoY, predominantly driven by

higher deposit margins, partially offset by lower deposit-

related fees

Payments revenue of $2.2B, up 79% YoY

Investment Banking and Markets revenue, gross of

$767mm, down 3% YoY

• Expense of $1.3B, up 12% YoY, predominantly driven by

higher compensation, including front office hiring and

technology investments, as well as higher volume-related

expense

Credit costs of $489mm

• Reserve build of $389mm, driven by updates to certain

assumptions related to office real estate, as well as net

downgrade activity in Middle Market

• NCOs of $100mm, predominantly driven by office real

estate

Average loans of $242B, up 10% YoY and up 2% QoQ

C&I7 up 14% YoY and up 2% QOQ

● CRE7 up 7% YoY and up 1% QOQ

Average deposits of $275B, down 8% YoY, driven by

continued attrition in non-operating deposits, but up 3% QOQ,

driven by inflows from new client acquisition, partially offset

by continued attrition in non-operating deposits

7View entire presentation