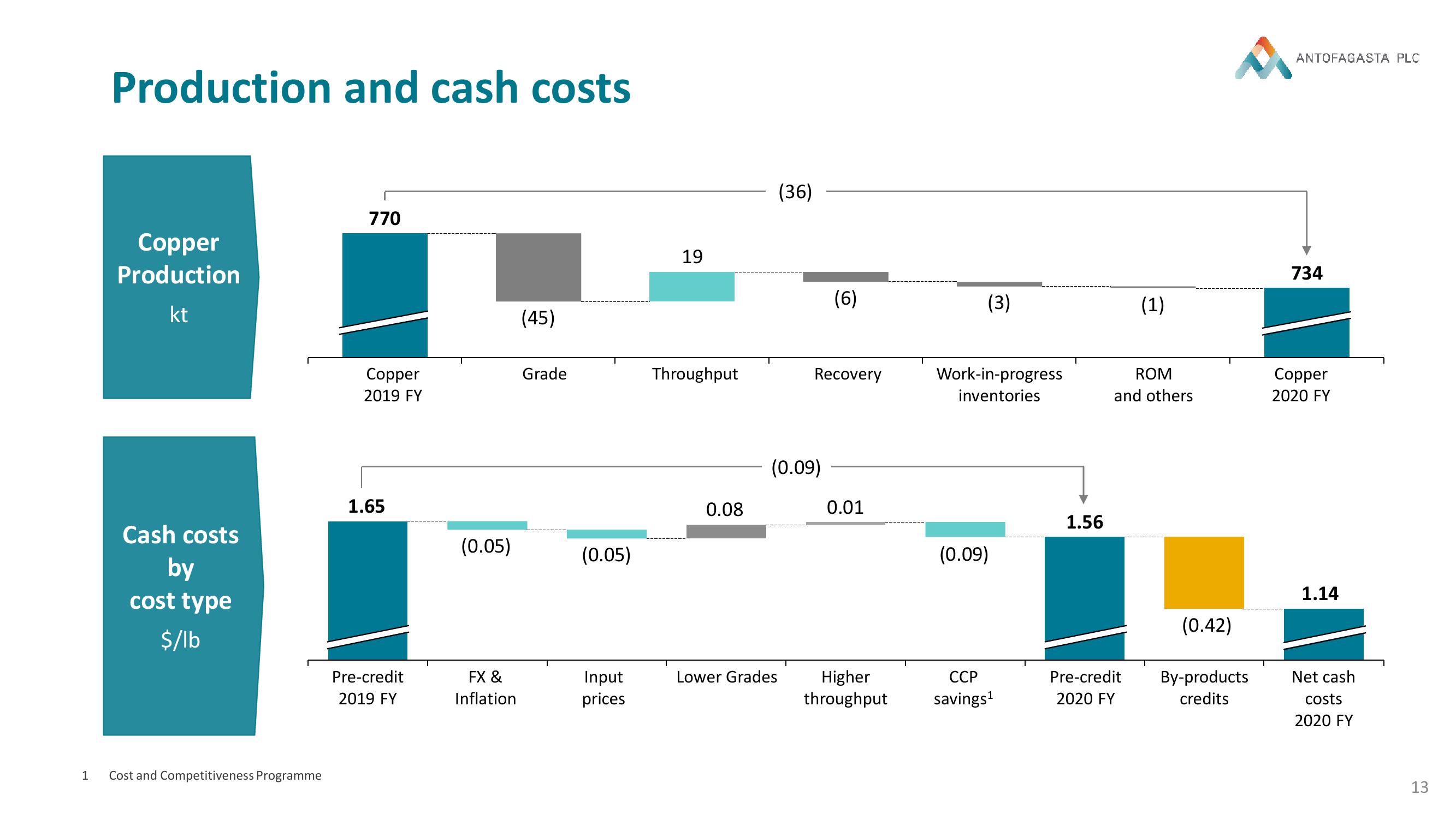

Antofagasta Results Presentation Deck

14 of 36

Slides

Transcriptions

Download to PowerPoint

Download presentation as an editable powerpoint.

Related

Freightos Results Presentation Deck

Industrials

Hexagon Purus Results Presentation Deck

Industrials

Moelis & Company Investment Banking Pitch Book

Financial Services

Lumen Investor Day Presentation Deck

Communication Services

Context Therapeutics Investor Presentation Deck

Healthcare

Evercore Investment Banking Pitch Book

Financial Services

Marti Results Presentation Deck

Technology

UBS Results Presentation Deck

Financial Services